April 21, 2024

by Scott Martin | Apr 21, 2024 | Weekly Newsletter 7pm Sunday

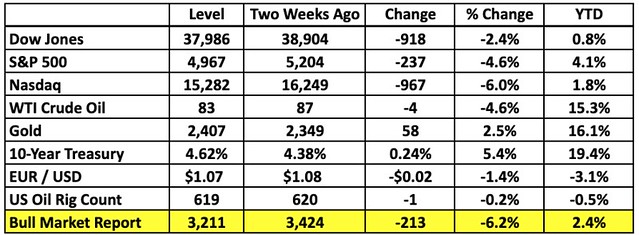

Market Summary

The Bull Market Report

While some investors are convinced that September and October are the cruelest months, this year we're seeing April play out as a stormy season. Our stocks have stepped a collective 6% back since the month started, giving back nearly all their once-substantial YTD gains. Likewise, the Nasdaq and the Dow Industrials have also seen their 1Q rally evaporate, leaving both indices along with us on the brink of breakeven. Only the S&P 500, as middle-of-the-road as it gets in the modern market, is showing the bears any resistance whatsoever, and it's still down 5% so far this month.

People can blame the bond market for this, but in our view the situation is both more complicated and so simple that it needs little explanation at all. The last time stocks shuddered like this, nobody knew whether the Fed was finally done raising short-term interest rates, which ensured that there was still enough anxiety circulating to keep investors off balance. We had a pretty good sense then that the Fed's "pause" would continue for the foreseeable future, but nobody had the confidence to say for sure. As a result, money flooded out of the Treasury market into higher-yielding cash, leaving bond prices reeling and pushing yields up to 5% in the process.

A similar dynamic has played out this time around. The mood around the Fed has gotten significantly softer, with investors who had once hoped for nothing better than an extended end to rate hikes starting to bet more confidently on active rate cuts in the coming year. However, even that improved attitude is vulnerable to second guessing and frustration when the economic numbers flow the wrong way. As long as inflation remains stubbornly persistent, the Fed's calculus around rate cuts in the near term will remain difficult, and the hope that dominated the market early in the year gives way again to doubt.

That's the complex narrative. But when you look at the way stocks and bonds have moved in the last six months, you'll see a much simpler pattern emerge. Bond yields got so high in November that they started to strain the statistical limits, triggering an inevitable bounce when conditions finally reached an unsustainable level. When that happened, yields dropped and stocks rebounded. There wasn't any deep narrative going on here. It was just statistics. And then, around the new year, yields had swung all the way from testing the statistical ceiling to crawling on the floor, pushing markets in the opposite direction in response.

Again, just statistics. Money followed its own cyclical tide and human beings scrambled to tell the tale. The Fed didn't get in the way. A few weeks ago, markets were in roughly the same position as they were back in November. The cycle played out again. The earnings reports we'll review in the next few weeks may accelerate the ongoing correction; or give investors a strong enough reason to defy statistics and start buying again. For now, however, we're resigned to see stocks drift a little while before regaining their equilibrium. All part of life on Wall Street.

At moments like this, we look for pockets of relative strength and weakness to make sure we're positioned the right way to exploit the market's next moves. The fact that the losses are relatively evenly distributed tells us that this is not a problem for the economy or any particular sector. Our Healthcare recommendations are down roughly as much as our High Yield stocks this month, and the REITs and Stocks For Success have also experienced roughly the same level of pain in the last few weeks. When such a large slice of the market drops at the same speed and correlations across otherwise unrelated industries converge, the normal pattern of distributed strength and weakness disintegrates. There's no shelter, in other words. Defense and offense, established companies and speculative ones are all moving together.

That's the kind of move that tends to reverse itself in the pattern we've watched since November. In the meantime, we appreciate our Energy portfolio more than ever, as well as our allocation to SPDR Gold Shares (GLD). Gold is a hedge when everything else is suffering. That's why we're happy to be in gold right now.

There's always a bull market here at The Bull Market Report. With earnings season just underway, The Big Picture lays out where the growth is across the market and where we can anticipate it. The Bull Market High Yield Investor is all about making sure the yields we've gotten in the past will continue, which is important when the Fed keeps rates higher than a lot of investors think they can stand. And as always, we're talking about a few of our favorite stocks, including a few that have the power to change the market's mood when they report over the next few days. Don't forget: if you'd like different coverage or more detail on any topic, you know how to reach us. (Todd@BullMarket.com 970.544.1707).

Key Market Indicators

-----------------------------------------------------------------------------

The Big Picture: Where The Growth Is

-----------------------------------------------------------------------------

BMR Companies and Commentary

Axcelis Technologies (ACLS: $95, down 9% last week)

High Technology Portfolio

Axcelis Technologies designs and manufactures critical equipment for the $550 billion global semiconductor industry. It recently released its fourth-quarter results, reporting $310 million in revenue, up 17% YoY, compared to $270 million a year ago. It posted a profit of $70 million, or $2.15 per share, against $65 million, or $1.99, with a beat on consensus estimates on the top and bottom lines.

As the global semiconductor boom accelerates, Axcelis continues to see strong demand for its Purion Power Series product family, hitting $1.2 billion in order backlogs to end the year 2024. This can largely be attributed to the semiconductor nationalism, aimed at reducing dependence on Taiwan and minimizing the supply chain risks that come with the same. In addition to this, Axcelis is currently riding on the coattails of many other tailwinds, ranging from the electrification of the automotive industry to the global rollout of 5G, IoT, IIoT, and AI, among others. The company generates 98% of its revenue from the ion implantation market, where it maintains a strong portfolio of products, alongside substantial blockades leaving it with very few worthy competitors.

The stock, alongside the company’s performance, cooled off substantially over the past year, and much of this can be attributed to the rationalization of capital expenditure in the industry. Apart from this, China, where Axcelis generates 46% of its revenues, was been hit with a prolonged slowdown. However, now that the country is starting to turn around once again, we expect robust demand going forward.

After surging 140% in the first half of 2023, the stock has shed more than half its value from its all-time high of $201 last summer, currently down 24% year-to-date. This creates an interesting situation: a growth stock with a compelling valuation, trading at under 3 times sales and 12 times earnings, especially as it begins returning capital to investors with $15 million in buybacks during the quarter. With $510 million in cash, just $45 million in debt, and $160 million in cash flow, the company is poised for strong future growth in this industry that is roaring on all engines. The Target is $200 with a Sell Price of $105, both of which should be adjusted today. The stock is sitting now where it was a little over a year ago. In 2021, the stock was at $30. So let’s look at revenues and earnings.

| Year |

Revenue |

Earnings |

| 2023 |

$1.15 billion |

$250 million |

| 2022 |

$920 million |

$180 million |

| 2021 |

$660 million |

$100 million |

Note that the company is still tiny compared with the big boys in the industry, with a market cap of just $3 billion. The company might just be on the buyout list of many companies in the business.

We are moving the Target to $150 and the Sell Price to $75.

-----------------------------------------------------------------------------

Bill Holdings (BILL: $60, down 3%)

High Technology Portfolio

Financial management platform for small and medium-sized businesses, Bill posted its second-quarter results recently, reporting $320 million in revenue, up 20% YoY, compared to $260 million a year ago. It posted a profit of $70 million, or $0.63 per share, against $50 million, or $0.42, with a beat on consensus figures on the top and bottom lines, coupled with robust guidance for the third quarter and full year.

The company generates the bulk of its revenues from subscriptions and transaction fees, at $275 million, up 19% YoY, followed by float revenue, which is interest earned on client deposits, at $43 million. The latter number was a significant increase in recent years owing to higher prevailing interest rates. During the quarter, the company processed $75 billion in payments, across 26 million transactions, up 11% and 23%, respectively. The platform now hosts 470,000 small and medium-sized businesses located all across the world, up 19% YoY, alongside 5.8 million network members, 7,000 accounting firms, and 7 out of the 10 largest financial institutions, resulting in a strong barrier to its competition.

The company saw a marked slowdown in its growth rate, from 65% YoY in 2023 to just 20% during this particular quarter. This is owing to its significant macro exposure, and the prevailing broader slowdown, coupled with the company hitting a saturation point in certain regards. Its next stage of growth will come internationally, where it has an addressable market of over 330 million businesses.

Despite an 82% pullback in the stock from its all-time high in 2021, it still features a fairly expensive valuation of 5 times sales and 21 times earnings. During the quarter, the company returned $200 million to investors in stock buybacks, made possible by its $2.6 billion in cash reserves, $1.9 billion in debt, and $250 million in cash flow. Our Target is $85 and our Sell Price is $50. The company produced strong growth in revenues, having done $240 million in fiscal 2021, $640 million in 2022, and $1.05 billion in 2023. It appears that revenue for the fiscal year that ends June 2024, will total about $1.2 billion, quite a slowdown, just 16-18% growth when we have been used to 50%+ growth.

Bill Holdings has a $6 billion market cap, quite a comedown from the $36 billion it hit in 2021. Do we want to hang with the company now after this comedown? That’s a good question and one that you have to ask yourself as well. We like companies that are growing 30% a year or more, but perhaps we are entering a different dynamic lately and should be pleased with 15-20% growth. We’re going to stick with the company for a little bit longer but watch it closely. If the stock moves to the $55 level, our new Sell Price, we are moving on.

-----------------------------------------------------------------------------

PayPal (PYPL: $62, down 4%)

Financial Portfolio

Global payments giant PayPal released its fourth quarter results recently, reporting $8.0 billion in revenues, up 9% YoY, compared to $7.4 billion a year ago. It posted a profit of $1.6 billion, or $1.48 per share, against $1.4 billion, or $1.24, beating consensus figures on the top and bottom lines. The company, however, disappointed some on Wall Street, with its guidance for the coming year, at 6.5% revenue growth, making us think long and hard about the future of this investment. For the year, the company did $30 billion in revenue, up 8%, up 75%(!), with $4.2 billion in profits. The is no small company, clocking in at $65 billion in market cap.

The numbers are certainly big. During the quarter, the company’s payment volumes hit a record $410 billion, up 15% YoY, and $1.5 trillion for the full year, up 13% YoY. This was driven by a 14% YoY rise in total transactions per account, at 59, helping offset a slight decline in the total active accounts on the platform at 426 million, down 2%. This was largely the result of the company ending its extensive promotions involving bonuses and cashbacks.

Two years ago, PayPal was forced to manually close over 4 million accounts in response to massive promo fraud and abuse. It marked a shift in the company’s marketing strategy, and the repercussions of this are being felt to this day. It is now focused on the quality of accounts, rather than merely focusing on fresh new accounts opened, and it seems to be working well given the positive metrics that have resulted.

PayPal introduced several new services and initiatives in recent months, the most promising of which is its PYUSD stablecoin, designed to make international payments a lot smoother. It allows users to transfer US dollars to over 160 countries, without incurring any transaction fees, marking the company’s biggest foray into cryptocurrencies, in the $150 billion stable currencies market.

Following an 80% pullback since its all-time high in 2021, the stock trades at an enticing valuation of just 2.3 times sales and 12 times earnings. With a string of new products, services, and initiatives around the corner, extensive restructuring, and $5 billion in buybacks, we expect strong value creation in the months ahead. It ended the quarter with $14 billion in cash, $12 billion in debt, and $5 billion in cash flow. Our Target is $75 and our Sell Price is $48, hereby raised to $54. We’ve been with this company a long time, having added it at $31 in 2016. We’re looking at a 100% return which is fair, but the return was a lot better by 2021, three years ago, when it hit $310. Will it ever return to its glory days? Tough question. At this level and valuation, we have a company that is growing (revenues of $21 billion in 2021, $30 billion in 2023), with strong profits each year. We like this company and would suggest you stick with it and add to it as it moves higher (or lower – either way a winning strategy). The company is a leader, is strong financially, and will come out on top as we move into the 2nd half of the roaring 2020s.

-----------------------------------------------------------------------------

Shopify (SHOP: $70, flat)

High Technology Portfolio

eCommerce platform Shopify had a phenomenal fourth quarter to cap off an impressive year, posting $2.1 billion in revenue, up 24% YoY, compared to $1.7 billion a year ago. The company posted a profit of $440 million, or $0.34 per share, against $93 million, or $0.07, beating consensus estimates on the top and bottom lines, yet investors were dismayed with the light guidance provided for the new year.

The company’s merchant solutions segment led the way with $1.6 billion in revenue, up 21% YoY, followed by subscription solutions at $525 million, up 31% YoY. This was driven by steady growth in gross merchandise volumes and payments, at $75 billion and $45 billion, up 23% and 32% YoY, respectively, as Shopify penetrates deeper into the commerce value chain while being aided by a resilient US economy.

Shopify unveiled many new products and services during the quarter, starting with Shopify Magic, its suite of new AI tools to help run stores more efficiently. This was followed by Sidekick, its AI-enabled commerce assistant, and its new ChatGPT-powered shopping assistant for consumers, all aimed at unlocking value for merchants on the platform, and helping them go toe-to-toe against larger retailers.

The platform now powers 11% of all e-commerce sales in the US, an amazing number when you concentrate on it, and has endless potential for further growth, both in the US and internationally. What began as a solution for small businesses to set up online storefronts with ease turned into the platform of choice for large B2B and consumer brands, including the likes of AllBirds, Mattel, and Carrier among others.

Let’s take a moment to discuss what makes Shopify such a great company:

Shopify's success stems from a combination of factors for both e-commerce businesses and investors. Here's a breakdown of its strengths:

Ease of Use and Scalability

Simple Interface: Shopify boasts a user-friendly platform that allows entrepreneurs with minimal technical expertise to set up and manage their online stores.

Scalability: As businesses grow, Shopify scales with them. They can adjust their plans and add features seamlessly to accommodate increasing needs.

Wide Range of Features and Integrations

Built-in Features: Shopify offers a comprehensive suite of features for managing products, inventory, payments, shipping, marketing, and analytics.

App Store: The Shopify App Store provides access to thousands of additional apps and integrations, allowing businesses to customize their stores and extend functionality.

Strong Ecommerce Ecosystem

App Developers: A thriving app developer community constantly creates new extensions and tools for the Shopify platform.

Payment Gateways: Integrates with various popular payment gateways, offering flexibility for customers.

Support Resources: Provides extensive documentation, tutorials, and a supportive community for troubleshooting and learning.

Focus on Merchants

Affordable Pricing: Offers tiered pricing plans to cater to businesses of all sizes, making it an attractive option for startups and growing companies.

Success Stories: Shopify showcases success stories of merchants who have thrived using their platform, inspiring new entrepreneurs.

App Marketplace Revenue Sharing: Shares a portion of revenue generated by third-party apps with Shopify merchants, incentivizing app development for the platform.

Market Leader and Growth Potential

Market Share: Shopify is a dominant player in the e-commerce platform market, attracting a large user base and benefiting from network effects.

Constant Innovation: They continuously invest in research and development, introducing new features and expanding their offerings to stay ahead of the curve.

Global Presence: Shopify operates in a vast market with significant growth potential, particularly in developing economies.

Despite a 120% rally last year, the stock is still down by nearly 60% from its all-time high of $176 in 2021, while featuring an undeniably expensive valuation of 13 times sales and 70 times earnings. These figures are, however, well justified given its 20%+ YoY growth, and a 5-year CAGR of 40%. The company ended the quarter with $5 billion in cash, just $1.2 billion in debt, and $1.0 billion in cash flow. Our Target is $100 and we would not sell Shopify. We would suggest an over-allocation of this company in your portfolio. We believe in Shopify big time.

-----------------------------------------------------------------------------

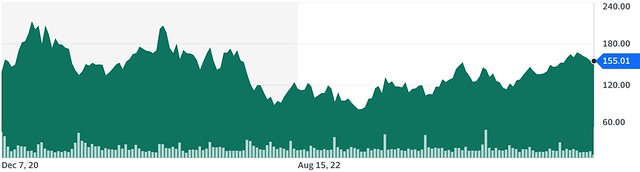

Airbnb (ABNB: $155, down 3%)

Long-Term Growth Portfolio

Vacation rental giant Airbnb ended the year on a high note, with its fourth-quarter results, reporting $2.2 billion in revenue, up 17% YoY, compared to $1.9 billion a year ago. The company posted a loss of $350 million, or $0.55 per share, against a profit of $320 million, or $0.48, with a miss on earnings, but a beat on top-line consensus estimates, with strong guidance bringing respite for investors. The loss during the quarter was the result of a $620 million tax settlement with the Italian government, which amounts to 41% of its net profits for the full year. This, of course, is a one-time expense, and the company will return to profitability in the coming quarters. Other operating metrics and Key Performance Indicators were impressive, to say the least, hinting at a rebound in global and domestic travel.

Gross booking values hit a fresh high of $15.5 billion in the quarter, up 15% YoY, and a mammoth 80% since 2019, driven by a total of 100 million nights booked on the platform, up 12% YoY. With its new initiatives aimed at helping hosts unlock more value, the platform added a record 1.1 million new listings during the past year, up 18% YoY, bringing its total active listings to 7.7 million located around the world.

Airbnb was been faced with a few challenges and headwinds in recent years, starting with regulatory scrutiny, the ban in New York City, and intensifying competition. It is, however, working hard and succeeding in differentiating itself, much of which involves its new focus on creating experiences, not just renting rooms. This, coupled with its new AI-assisted booking tools gives the company an upper hand against competitors.

Going forward, the company will be unlocking value across its massive landed base of hosts and guests. As of now, it is in a sound financial position, with $10 billion in cash reserves, $2.3 billion in debt, and $3.9 billion in cash flow. In light of this, the company announced a fresh $6 billion stock buyback program, adding further support to its 15% rally YTD. Our Target is $195 and our SP is $125. This company has been changing the world as we know it, and we are here to say that it will continue to change the world of travel and experiences. At $100 billion in market cap, this is no small company. We expect it to hit new all-time highs ($214) in 2025 or 2026. Many very intelligent minds on Wall Street have large positions in the stock. You should too.

-----------------------------------------------------------------------------

Netflix (NFLX: $555, down 11%)

Long-Term Growth Portfolio

Streaming giant Netflix released its first quarter results last week, reporting $9.4 billion in revenue, up 15% YoY, compared to $8.2 billion a year ago. The company posted a profit of $2.3 billion, or $5.28 per share, against $1.3 billion, or $2.88, while blowing past estimates on the top and bottom lines. The stock ran into a bad day on Wall Street Friday and fell with big boys – Microsoft, Google, Facebook, Nvidia, Super Micro Computers, and others. But let’s put this in perspective. The stock was at $328 a year ago. It was at $555, its current price, two months ago in February. So a little pullback doesn’t faze us in the slightest. The numbers that the company produced are really all that matters. Take a look, below, at the new subscribers the company added in the quarter.

The company did remarkably well across a host of other metrics, starting with net new subscribers at an amazing 9.3 million, up from just 1.8 million a year ago, driven by its crackdown on password sharing and other initiatives. Total memberships on the platform closed in on 270 million, up 16% YoY, and well ahead of Street estimates at 264 million. Netflix, however, believes that subscriber growth is no longer its primary focus as it was all this while, with revenue, margins, engagement, and customer satisfaction taking its place. The company plans to phase out the reporting of its quarterly membership figures, a plan that hasn’t gone over well with investors, but this pullback was an overreaction nonetheless. The move to stop sharing membership figures each quarter was done with the same in mind. We are disappointed about this decision, but we’ll have to live with it. We’ll just have to watch revenues and profits even more closely, which is really what it’s all about anyway.

Netflix’s next stage of growth will come from monetizing its massive landed base and network effects, and the launch of its ad-supported pricing tier. Its foray into live sports streaming and video games was done in pursuit of the same. Other avenues include theatrical releases of select content to recoup its investment, merchandising, and product placements which have remained underutilized.

Despite the pullback last week, the stock remains up 18% YTD and 70% over the past year, while trading at a valuation of under 8 times sales and 32 times earnings. During the quarter, the company repaid $400 million in debt, while repurchasing stock worth $2 billion, made possible by its increasingly robust balance sheet position with $7 billion in cash, $17 billion in debt, and $7.3 billion in cash flow. Our Target of $590 was hit after the stock ran up to $638 in early April. Have no fear – that number will be seen again in the coming months. We’re raising our Target to $650 and our Sell Price remains: we would not sell Netflix.

-----------------------------------------------------------------------------

Blackstone (BX: $118, down 4%)

Stocks For Success Portfolio

Private equity giant Blackstone released its first quarter results last week, reporting $2.6 billion in revenue, up 2.6% YoY, compared to $2.5 billion a year ago. The company posted a profit of $1.3 billion, or $0.98 per share, against $1.2 billion, or $0.97, with a marginal beat on earnings and a slight miss on the top line. Business as usual for the largest manager of assets in the world. Fee-related earnings during the quarter stood at $1.2 billion. Fresh inflows stood at $36 billion, down 36% from the prior quarter and 16% YoY, but impressive nonetheless, considering its size. Its uninvested capital has now reached $190 billion.

All of Blackstone’s core funds posted strong performances during the quarter, with its core and opportunistic real estate funds gaining 1.0%. This was followed by its corporate private equity and infrastructure funds, up by 3.4% and 4.8%, and finally, its credit and hedge funds appreciating by 4.1% and 4.6%, respectively, which are impressive figures. This performance has been driven by strong global equity markets, coupled with an end to the Fed’s hawkish stance, reigniting mergers and acquisition activities that had come to a standstill over the past 18 months. The central bank remains non-committal on further rate cuts, which should help the market move forward on the deal-making front going forward.

Why Blackstone is a Leader:

- Experienced Team: Blackstone has a team of seasoned professionals with deep expertise in various investment sectors. This expertise allows them to identify promising opportunities, manage risk, and generate strong returns for their clients.

- Strong Track Record: Their long history of success and consistent performance have earned them a reputation for excellence in the alternative investment industry.

- Scale and Resources: The sheer size of their AUM allows them to access exclusive deals, negotiate better terms, and attract top talent, further strengthening their position.

- Focus on Innovation: Blackstone actively explores new investment strategies and asset classes, staying ahead of the curve and adapting to evolving market trends.

- Client Focus: They prioritize understanding their clients' investment goals and risk tolerance, tailoring solutions that meet their specific needs.

Overall, Blackstone's combination of a diverse range of alternative investments, a highly experienced team, a stellar track record, immense resources, and a commitment to innovation makes it a dominant force in the alternative investment landscape.

The stock is down 8% YTD, following a 76% rally last year, but we cannot discount its potential for consistent fee income, from its $1.06 trillion in assets under management. Blackstone returned $1.2 billion to investors in buybacks, in addition to its annualized yield of 3.6%.

It’s been a good investment for us. We added the stock at $27 in 2016 and we have a Target of $150 on the stock. We would not sell Blackstone. The firm has the best asset managers in the world and that allows stockholders to sit back and let them do their thing.

-----------------------------------------------------------------------------

Alphabet (GOOG: $156, down 2%)

Stocks For Success Portfolio

Reporting Earnings This Week!

While revenues and profits continue to scale unabated, Google parent Alphabet has had an undeniably rough couple of months. On the heels of its first quarter results this week, some investors remain ill at ease, with the company firmly on the backfoot on the AI front, trailing behind competitors such as Microsoft, which is making massive strides in collaboration with OpenAI across its suite of products and services. Note that we at The Bull Market Report are not some of those investors who are ill at ease with this great company.

Google has introduced the world to Gemini, its generative Artificial Intelligence entry into the competition for the world’s eyeballs. Have you tried it yet? Powerful beyond words. Plus, the company still has remarkable moats, with integrations across platforms, browsers, and devices. Whether it is ChatGPT itself, or Microsoft’s Bing search engine with the new AI tool, Copilot, neither can build the kind of ecosystem that Google has painstakingly acquired over the years. Stay tuned for a NewsFlash on Alphabet after earnings are released on Thursday after the close.

-----------------------------------------------------------------------------

Microsoft (MSFT: $399, down 5%)

Stocks For Success Portfolio

Reporting Earnings This Week!

Tech giant Microsoft is doing everything right of late, and its market cap of $3 trillion at 30 times earnings reflects the same. Certain analysts and observers are concerned that this AI-driven exuberance is set to burst, but this is remarkable shortsightedness that comes from traditional valuation models which fail to factor in the remarkable disruptive and value creation potential of the latest advances in AI.

Just last week, the company released a research paper on AutoDev, its new framework for automated AI-driven coding. This framework will make manual coding a thing of the past, and bring application development to individual managers, as opposed to large teams. Software development jobs in the future will be more management and supervising of AI, rather than coding and development.

The company is set to release its third-quarter results after the close on Thursday, and more than its earnings and beat on consensus figures, we are looking forward to its next big exploits on the AI front. Microsoft made groundbreaking advances in AI in 2023, and we expect this momentum to continue unabated this year, as it unveils its growing prowess in this field across its massive portfolio of products and services. Stay tuned for a NewsFlash on Microsoft later this week after earnings are released.

-----------------------------------------------------------------------------

The Bull Market High Yield Investor

Concerns about persistently high inflation locking the Fed into high interest rates have rattled the bond market in particular but stocks are also feeling the pressure, seemingly confirming the common belief that once rates cross a certain threshold the environment gets toxic fast. But here's the reality: Going back across the past four decades, whenever 10-year Treasury yields spiked above 6%, the S&P 500 delivered an average annual return of 14.5%, compared to a less exuberant 7.7% return in years when bonds were paying less than 4%.

As it turns out, stocks performed better during periods of rising interest rates, with an average annual rolling one-year return of 13.9% as opposed to 6.5% in a falling rate environment. That probably isn't our world right now, but it supports the way the market has resisted its most bearish impulses as the economy adjusts to the Fed's most aggressive moves.

Remember, lower rates can often signal sluggish economic growth. The Fed cuts in the face of looming disaster and stays there until they’re 100% sure we’ve averted disaster. As a result, higher rates may actually reflect a stronger economy and the prospect of better corporate earnings, factors that usually bode well for the stock market. What's going on now?

Bond yields have been climbing since April, with the 10-year Treasury yield peaking near its highest level since November. This coincided with a decline in the S&P 500.

However, in our view, this anticipates a “return to normalization” with yields eventually settling around their 75-year average of 5%. You read that right. Rather than being some toxic frontier, 5% is average. It’s normal. And it’s really just about 2 percentage points above ambient inflation. If the Fed coaxes price pressure back down to its target, that translates to bond yields staying at or above 4%.

But the most important thing here is that the world didn't end in November, which is the last time long-term rates got this high. Unless something fundamental has broken in the last 5-6 months, the world is unlikely to end now. What matters to us is where the bond market starts paying a high enough yield to become a compelling alternative to dividend-paying stocks. Right now, we aren't especially impressed with anything less than 2 percentage points above ambient inflation, which eliminates just about the entire Treasury market from serious consideration.

Yields need to get higher to give stocks or even cash a run for their money. That means the bond market is in for more pain. And in that scenario, the risk-return calculations favor our High Yield recommendations as a place to park money and earn income at relatively low risk. They might not have the same near-zero risk profile as federal debt, but they make up for it by offering investors a chance to collect additional upside over time. Bond returns are fixed if you hold them to maturity. Stocks are always a work in progress, where we sacrifice certainty (nothing is "fixed") in exchange for a potentially richer long-term return.

However, our ability to say that with any degree of confidence requires some sense that dividends will keep coming. Congressional bickering aside, there's no threat that Treasury bonds will fail to pay the rate you lock in when you buy them. But if you can't count on your stocks to at least keep their dividends where they are, there's no clarity there at all. You want to know that your portfolio can pay the bills. If something starts to look like it isn't working, it needs to go. That's where we are now with one of our holdings.

BlackRock Income Trust (BKT: $11.37, up 1%. Yield=9.3%)

REMOVING FROM ACTIVE COVERAGE

A leading closed-end fund with exposures to mortgage-backed securities as well as US government treasuries, BlackRock Income Trust had been on an ascendant streak since the latter half of last year, but this momentum has since fizzled out. Yet, none of this should matter to conservative, income-seeking investors, with a long enough time horizon, given the fund’s remarkable yields.

The trust’s rally starting mid-last year was largely the result of the Fed ending its hawkish stance, and embarking on rate cuts for the first time in two years. Things, however, have changed in recent weeks, with the Federal Reserve now seemingly in no hurry to cut rates any further, resulting in a pullback in the stock, and leaving it down by 8% YTD.

The Trust invests in AAA-rated securities, backed by government agencies such as Fannie Mae and Freddie Mac. As interest rates rise, bond prices go down, and the stock trades at a discount to book value – currently 11%.

The trust is struggling to cover its distributions as of now, and analysts fear that a dividend cut is around the corner. This has put pressure on the stock and will put more pressure on the stock.

The stock has been a laggard for quite some time now. In the last 12 months, the stock is down 8% and there is some conjecture that the firm may have to cut its dividend. If that happens we can see the stock drop another 8% in the following month. We don’t want to take this risk so we would suggest a sale of the stock at this point. We are thus removing the stock from coverage. The investment hasn’t been a good one for us. We added the stock at $18.33 in 2019, and we should have gotten out a long time ago.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

May 7, 2023

by Scott Martin | May 7, 2023 | Weekly Newsletter 7pm Sunday

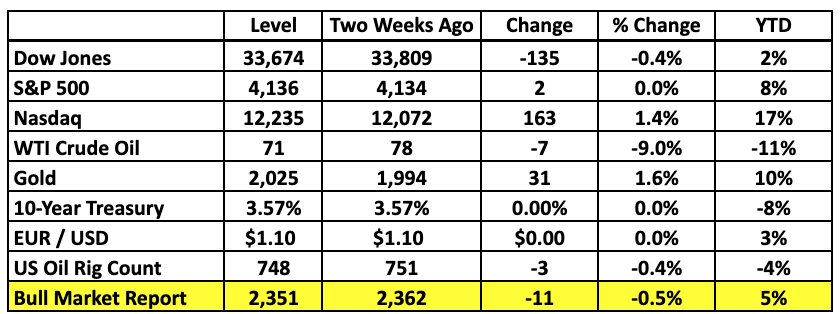

Market Summary

A few traders threw a tantrum last week after Jay Powell said "it would not be appropriate" to cut interest rates in the immediate future. We have to say that while a pause in rate hikes seems imminent, active cuts were vanishingly unlikely unless the banking system collapse. And that's not exactly something rational investors really should be eager to see. So instead of focusing on what it would take for the Fed to suddenly reverse its war on persistent inflation, we'd like to open this Bull Market Report with a survey of the facts on the ground.

The Fed has the best view of the economy and in fact determine its trajectory from month to month. They're effectively saying the sky is too blue and the sun is too bright for comfort. We can disagree with the Fed but they still call the shots. They aren't feeling stormy weather. They want it to get stormier. Over the years we've learned a lot about how Jay Powell thinks. He hates high interest rates. The thought of a severe recession that throws millions of people out of work terrifies him. He'll relax the minute inflation recedes to a tolerable level.

As far as our portfolios are concerned, the world does not appear to be ending, and because other investors keep bidding up many of our stocks, we once again have pockets of fresh profit, keeping our results stable in a month when the market as a whole struggled from time to time without surrendering. Despite all the talk about the Fed breaking things in the Banking industry, the S&P 500 actually managed to shake off all of its Silicon Valley losses to edge 0.2% above its February high just a few days ago.

That's an achievement that would otherwise get lost in the gloom. We like it when the market can support a pattern of higher highs because it means money keeps flowing into stocks across Wall Street's periodic mood swings. Without that virtuous cycle, the bulls simply wouldn't be able to climb each wall of worry. But that's exactly what's happened here. Admittedly, it took several weeks for that to happen and the breakthrough was only a handful of points on the S&P 500 before the latest round of Fed dread took it away.

We're still a long way from fully shaking off the bear's grip on the market. Every shock will stir sentiment and uncover remaining pockets of anxiety. But in every cycle since October, the bulls reach a little higher and the bears fail to push stocks so far down. Life, in other words, starts looking better from month to month. Companies not only learn how to survive shifting economic conditions but demonstrate that they can operate profitably. They're thriving. A lot of our stocks are thriving as well. That would not be the case if the economy were teetering on the edge of a cliff.

In the last two weeks, Energy took a significant step back. That's not a thrill for shareholders, but it's a pretty good indication that inflation is receding with commodity prices. Weaker inflation means the Fed can relax and act to comfort the market in a crisis. If you're afraid of the Fed, this is a good thing for every stock that doesn't make money pumping fuel out of the ground. And if you don't see that, then maybe the Fed isn't really what scares you. Meanwhile, the Financials are relatively resilient. Some innovative names like Bill Holdings (BILL) and PayPal (PYPL) are actually moving up, expanding their market footprint as entrenched legacy Banks falter.

This is how the economy works to create wealth at the expense of old broken ways of doing things. Our High Technology portfolio jumped 4% in the last two weeks. The core Stocks For Success group, dominated as it is by the biggest giants of Silicon Valley, also moved up. Microsoft (MSFT) rebounded 9% over this time period. Apple (AAPL) jumped 5%. Innovation is no longer seen as a problem or a source of empty hype. Serious investors are once again finding these stocks attractive because they represent a solution to the challenges that face us all.

But innovation isn't everything. People need places to live and work, no matter what virtual reality miracles happen in the "metaverse" or elsewhere online. Our Real Estate portfolio rebounded 5% in the last two weeks because the world failed to end. Big landlords didn't collapse. Believe it or not, their management teams have dealt with worse and didn't quit. They survived. And shareholders booked a lot of dividends over the years. That's another place wealth comes from.

There's always a bull market here at The Bull Market Report. This time around, we'd like to conduct a bit of a thought experiment in The Big Picture and take all the dread circulating around the market at face value. "What if," we ask, "the world isn't actually ending? What's the right investment posture for that?" The High Yield Investor takes a similar tone with a discussion of whether Jay Powell could have told the truth when he said the Banking system remains strong and relatively healthy. And as always, we have a lot of stocks to review. After all, it's earnings season. And the season is unfolding a lot better than many investors anticipated.

Key Market Indicators

-----------------------------------------------------------------------------

The Big Picture: "Normal" Is Right Here

We’ve all suffered through a lot together. The last few years have given investors the most jarring ride since the Great Recession. Banks are failing. The Fed seems obsessed with crashing the economy. A lot of people are convinced that the world is on the brink of collapse. The world can end in any number of ways, destroying endless wealth and security in the process. It’s enough to make someone head for the exits. But the question we need to grapple with as investors is a lot simpler: What if it doesn’t?

So let's run a thought experiment and postulate what would happen if the world stubbornly refuses to melt down and everyone on the sidelines misses their chance to participate in the good things the future still has in store. This scenario is not as outrageous as it might look. After all, the latest economic numbers suggest that the biggest immediate fear Wall Street and Main Street currently have to grapple with is the fear of missing out. While some corporations are trimming payrolls, enough are still hiring that unemployment keeps hovering around its lowest level in over 50 years. Wages are up. As the banks have revealed, households aren’t defaulting on their debt in large numbers. And as a result, the economy as a whole keeps growing just a little faster than inflation.

It might feel like a recession to weary workers. It might look like a recession on the horizon to wary investors. But there’s always a recession on the horizon . . . the cyclical nature of the economy ensures that we’re rarely more than a few years from the next one. And when the fundamental numbers keep trending in the bullish direction, experienced investors know that their portfolios will ultimately be worth more as well. That’s crucial in an inflationary world like the one we live in now.

Remember how the math works? When inflation is tracking at 3% over time, your wealth needs to earn at least 3% a year or you are actually losing purchasing power. You’re getting poorer. The Fed wants to drive inflation down to 2%, which is low but still just far enough above zero to penalize everyone so frightened that they can’t bear to do anything with their money beyond hiding it under the metaphorical bed. And right now, prevailing inflation remains high enough that even the highest-yielding bank products just don’t cut it.

That’s why the regional banks are failing, by the way. When their portfolios are stuffed with bonds paying less than inflation, they can’t raise the rates they pay on deposits. So depositors bail out and the balance sheets implode. But we aren’t banks. That’s actually not our problem. Our problem is how we effectively protect our existing wealth and build on it when the world fails to come to a screeching halt. That’s the problem of life. Living costs money. Unless the world comes to an end, you need to keep spending money.

Our solution starts with a little insurance against extended periods of market stagnation like the one we’ve just lived through. When your stocks go nowhere, you need a way to stay liquid. The biggest threat is outside circumstances forcing you to sell in stressed market conditions in order to pay the bills. That’s how hedge funds and retirement plans fail. Survivors keep enough cash flowing to surf the storms. Dividend stocks are a great way to do it. Our High Yield holdings focus on these opportunities to generate current income without selling a single share of stock. That’s our defense.

And anything less than an extreme outcome is temporary and partial by definition. Suddenly you aren’t facing the end of the world; you’re just looking at a stressful environment. Generations of history prove that Wall Street and Main Street alike have survived every shock and come back more resilient than ever. That’s the American way. On average, a year in the market is worth 8-11% above inflation. Some years are a lot worse and some are a lot better, but that’s the average that prevailed in the wake of the dotcom crash and the 2008 crash and even today. Over the past four years, the VIX has gone crazy and the Fed has spun in a vast and terrible circle. Recession and recession shadows have alternated with bear markets and bubbles. The market has still climbed almost exactly 11% a year on average over that period. Compounded.

Now maybe you’re eager to cut out some of the bad times in order to avoid the pain of a losing year for the market as a whole. We get that. Nobody enjoys stress. It isn’t the end of the world, but it can feel like it. Our solution there is equally simple. Nobody’s forcing you to buy and hold the market as a whole. There’s a whole world out there beyond the S&P 500. And there are always relative strong spots in the economy as well as obvious pain points. Last year, if you were brave enough to own Big Energy, you did well. We bought it. This year, Technology is coming back. You keep rotating. That’s life. It hasn’t ended yet. And we roll with the the changes and strive to beat the market averages.

-----------------------------------------------------------------------------

BMR Companies and Commentary

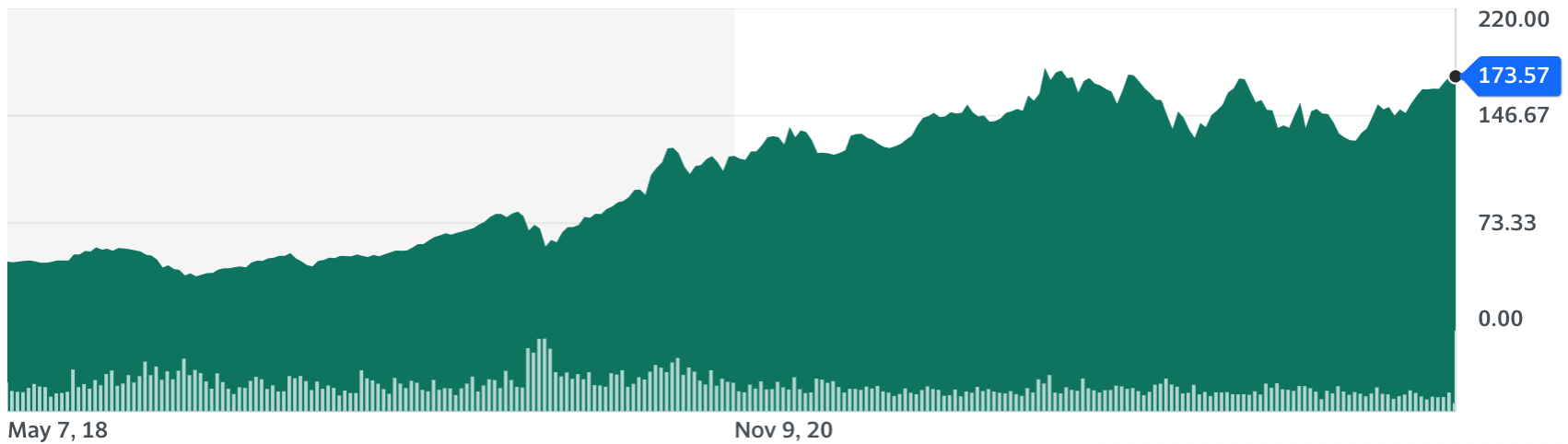

Apple Reports A Quarter That Pleases (AAPL: $174, up 2%)

Stocks for Success Portfolio

Amid bank failures, ceaseless rate hikes by the Fed and a global economy that continues to teeter on the edge of a recession (yet somehow manages from quarter to quarter never to actually fall over the cliff), Apple’s second-quarter results on Thursday were an absolute delight. The tech giant posted $95 billion in revenues, down 3% YoY, compared to $97 billion, with a profit of $24 billion, or $1.52 per share, down from $25 billion, or $1.52.

Despite posting its second straight quarterly drop in revenues, the stock popped 5% on Friday, thanks to the company’s beat on consensus estimates at the top and bottom lines. The stock has remained under pressure throughout the past three months, owing to rumors of a drop in Mac sales, coupled with the slowdown in fulfillment by its largest supplier, Foxconn, both of which were proven to be overblown during the results on Thursday.

The tech giant’s star performer remains its coveted iPhone, posting sales of $51.3 billion, up 1.5% YoY, compared to $50.6. The segment came in well ahead of estimates at $48.9 billion, even as worldwide smartphone sales contracted by over 15% during the same period. Apart from this, the Services business was the only other segment to post a YoY growth of 5%, with $20.9 billion in revenues.

Apple’s other key products - the Mac, iPad, and Other Products, which include wearables and accessories, posted a YoY decline. They each posted sales of $7.2 billion, $6.7 billion, and $8.7 billion, down by 31%, 13%, and 1%, respectively. The company, however, claims it witnessed a steady YoY growth across all key geographies, only to be weighed down by foreign exchange headwinds. We’re not sure we agree with the company on this last statement.

As to the future, the company expects a similar performance overall for the current quarter, as it continues to grapple with macroeconomic pressures, the slowdown in consumer spending, coupled with persistent supply chain issues. To address the latter, the company has gone all-out to diversify its sourcing and fulfillment away from China, in favor of India and Vietnam, among others for a more resilient supply chain. But getting there is a long process, as you can imagine.

In the face of growing challenges, Apple continues to remain the cash cow it has always been, with $29 billion in cash flow during the second quarter alone, of which nearly $23 billion was returned to shareholders in the form of dividends and repurchases. The company has authorized a further $90 billion in fresh repurchases, adding to the $600 billion in buybacks it has completed over the past decade. Now that’s a story!

In addition to this, the company raised its quarterly dividends for the 11th consecutive year, albeit, a small percentage. The company’s cash position continues to fall, at $51 billion at the end of this quarter, with debt of $110 billion, but this is hardly concerning given its remarkable cash flow. If you do the numbers, the firm is making almost $2 billion a week(!) Handing out cash to its stockholders is something the firm loves to do and will continue into the future.

The stock is flirting with its all-time high of $182 set in late 2021. Our Target for Apple is $190, which we are raising today to $220. The Sell Price is: We would never sell Apple.

-----------------------------------------------------------------------------

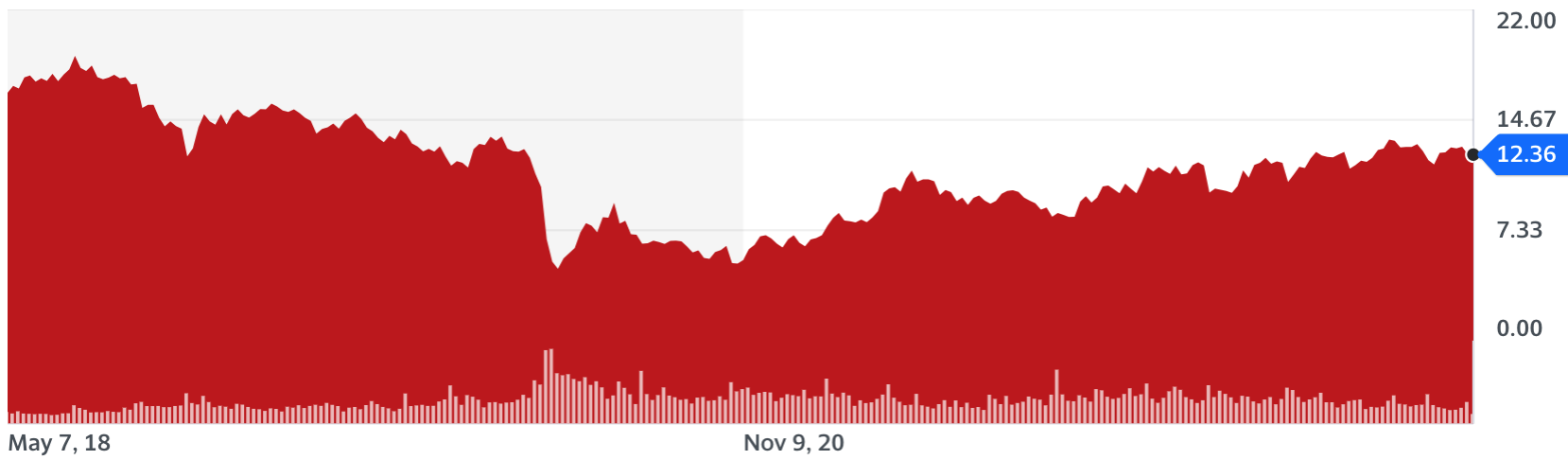

Energy Transfer (ET: $12.36, down 4%)

Energy Portfolio

Dallas-based Energy Transfer released its first quarter results early last week, reporting $19.0 billion in revenues, down 7% YoY, compared to $20.5 billion a year ago. The company posted a profit of $1.0 billion, or $0.32 per share, down from $1.2 billion, or $0.37, owing to lower energy prices and increased maintenance and operational expenses.

While the results were rather disappointing, in the case of midstream companies, top and bottom-line figures are largely irrelevant, given their vulnerability to energy price volatility. What matters is volumes, and in this regard, the company performed exceptionally well across the board, with its natural gas liquid fractionation and transportation volumes up by 18% and 13% on a YoY basis, respectively.

The midstream segment, interstate natural gas transportation, and crude oil terminal volumes were up by 14%, 11%, and 6% YoY, respectively. The growth in volumes is largely the result of the company’s Gulf Run Pipeline being placed in service, in addition to higher utilization across its Transwestern, Panhandle, and Trunkline systems, given the broad structural shifts being seen across the global energy markets.

We analyzed these trends thoroughly when we first started covering this stock last year, and to summarize it once again, it has to do with the rising rig counts within the US. With environmental concerns firmly on the back burner, the US is once again going all-out on domestic energy production, and as a result, midstream giants with extensive infrastructure are set to benefit from robust secular tailwinds. The company sports a $38 billion market cap.

Energy Transfer will continue delivering value to shareholders. This includes improving its balance sheet position, with $1 billion in debt pared down in the first quarter alone, aiming for a leverage ratio of 4 to 4.5x. Trading at just 0.44 times sales, it is remarkably undervalued for a stock boasting a yield of 10%, ending the quarter with $1.2 billion in cash, and $47 billion in debt.

The firm has a significant portfolio of long-term contracts in place. These contracts play a crucial role in ensuring stable revenue streams and mitigating price volatility risks. While specific details may vary, Energy Transfer typically enters into long-term agreements with producers, shippers, and end-users for the transportation, storage, and processing of natural gas, crude oil, refined products, and other commodities. A typical example of a long-term contract is a transportation agreement with a natural gas producer. Under this contract, Energy Transfer agrees to provide transportation services for a specified volume of natural gas over a period of 10 years. The contract stipulates a fixed transportation fee per unit of gas transported, providing predictable revenue for the company. Additionally, the agreement includes a minimum volume commitment, requiring the producer to ship a minimum amount of gas each year. Failure to meet the commitment may result in penalty payments. This long-term contract ensures a stable revenue stream for ET while offering the producer reliable transportation services for their natural gas.

Our Target is $14 and our Sell Price is $10. We would not hesitate to buy more at this level and could expect to see a 15-20% return per year in the future. Even if most of that is from dividends, it still counts as a win.

-----------------------------------------------------------------------------

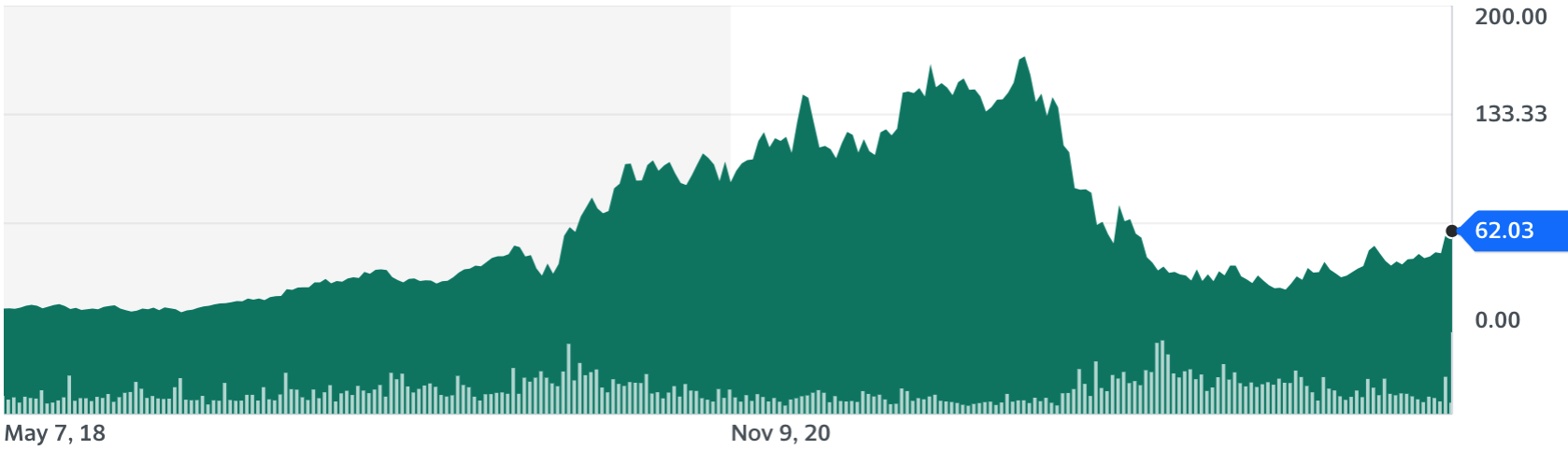

Shopify (SHOP: $62, up 28%)

High Technology Portfolio

eCommerce platform Shopify posted phenomenal first quarter results last week, reporting $1.5 billion in revenues, up 25% YoY, compared to $1.2 billion a year ago. The company posted a profit of $12 million, against $25 million last year. The unexpected beat on the top and bottom lines sent the stock higher following the results.

The company further continued its stellar streak across core operating metrics, starting with gross merchandise value at $50 billion, up 15% YoY, compared to $43 billion a year ago, followed by gross payment volumes at $28 billion, up 25% YoY, compared to $22 billion. Merchant and subscription solutions revenues came in at $1.1 billion and $380 million, up by 31%, and 11%, respectively.

Shopify had an eventful quarter, marked by significant additions of notable brands to its platform. The company witnessed a surge in the number of prominent brands choosing to utilize their e-commerce infrastructure and services. These brands recognized the value of Shopify's robust and user-friendly platform, which enables them to establish and grow their online businesses efficiently. It further announced the launch of Commerce Components by Shopify, a modern tech stack for enterprise retail, in addition to updated pricing across its basic and advanced plans, which went into effect for all new and existing customers two weeks ago.

The most important announcement, and one that came as a relief for shareholders and analysts, was the sale of its logistics business to Flexport, in return for a 13% stake in the firm. Given the nature, complexity, and laser-thin margins in this segment, this was a much-needed move, allowing Shopify to focus on its core competencies of building on its powerful e-commerce platform and network.

Shopify remains increasingly focused on profitability, as evidenced by the 20% cut in its headcount. Profits during the quarter would have been a lot higher, if not for the severance expenses of $150 million. The company’s balance sheet remains as robust as ever, with $4.9 billion in cash, just $1.6 billion in debt, and $100 million in cash flow, as it goes from strength to strength across its core businesses. We hold Shopify at the top of our list of investments for future growth. Our Target of $60 was hit this past week and we are raising it to $80 today. We would never sell the stock. The all-time high is $176, set in late 2021. This was the peak of its run from the $14 level in 2018. (We added it at $7 in 2017.)

SHOPIFY HAS A PLATFORM, like Facebook, like Apple’s App Store, like Google, like Amazon, and it is the most powerful tool in the world for young entrepreneurs to set up businesses and create wealth for themselves and their families. And when they succeed, the company takes part in their success. They are crushing the competition and will continue to dominate for decades to come.

-----------------------------------------------------------------------------

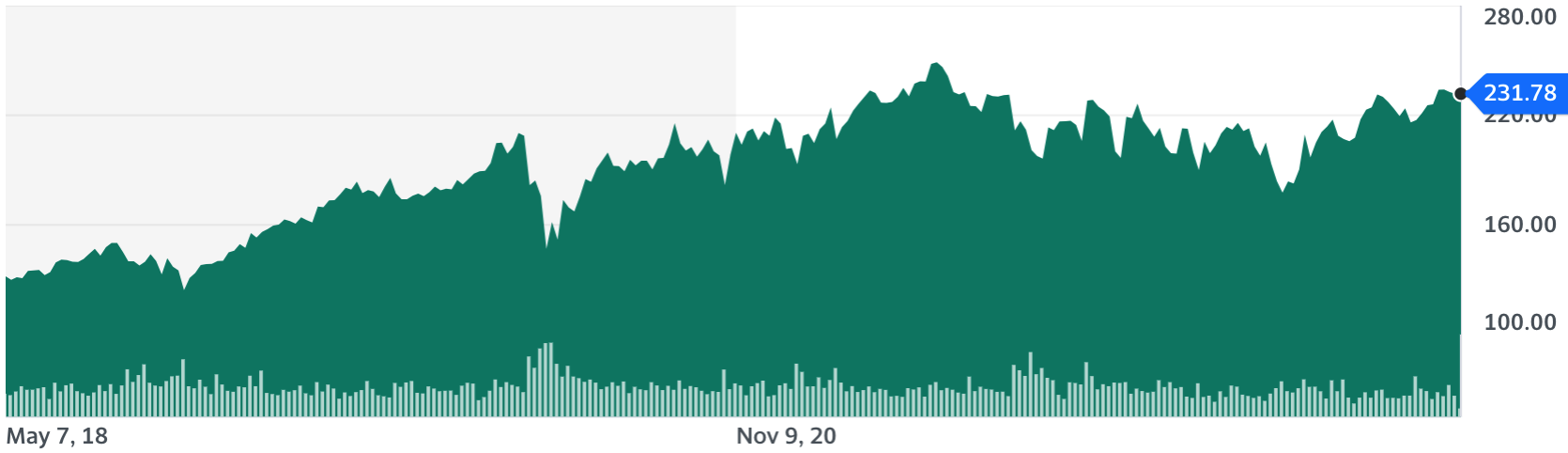

Visa (V: $232, flat)

Financial Portfolio

In the face of tough global macro conditions, payments giant Visa has continued to exceed expectations with its second-quarter results recently. The company posted $8.0 billion in revenues, up 11% YoY, compared to $7.2 billion a year ago, with a profit of $4.4 billion, or $2.09 per share, against $3.8 billion, or $1.88, with a huge beat on the top and bottom lines.

The company continued its stellar streak across core operating metrics, with payment volumes, cross-border volumes, and total payments processed, up by 10%, 24%, and 12%, respectively. This growth shows no signs of slowing down, with the double-digit growth across volumes, revenues, and earnings set to continue during the third quarter, thanks to its extensive dealmaking and ceaseless product innovation.

The global payments processing industry is essentially a duopoly dominated by Visa and Mastercard, both with wide moats keeping new entrants at bay. Visa currently has over 5 billion active debit and credit card accounts across 200 countries. The broad-based shift away from cash, and towards digital payments creates a robust secular tailwind for the company that is set to last throughout this decade and beyond.

Visa maintains this lead with long-term partnerships with leading financial institutions across the world, often with the help of incentives that cost as much as 27% of its gross revenues. During the second quarter alone, the company renewed agreements with the likes of TD Bank and CIBC*, among others. It further signed new card issuance deals with fintech companies Stripe and Adyen during the quarter.

* one of the largest banking institutions in the United States.

The most notable event during the quarter was the launch of Visa+, which represents the future of the company, offering instant peer-to-peer transfers across payment modes such as banks, PayPal and Venmo, wallets, apps, and more. The company continues to reward shareholders generously, with $3.2 billion in repurchases and dividends during the quarter, hardly making a dent in its balance sheet with $17 billion in cash, $21 billion in debt, and $19 billion in cash flow. Our Target is $265 and we would never sell the stock. The stock hit a 2-year high this past week. As this bull market continues, this stock will lead the pack and hit a new all-time high ($252), set in the summer two years ago. We can’t wait to raise the Target to $300.

-----------------------------------------------------------------------------

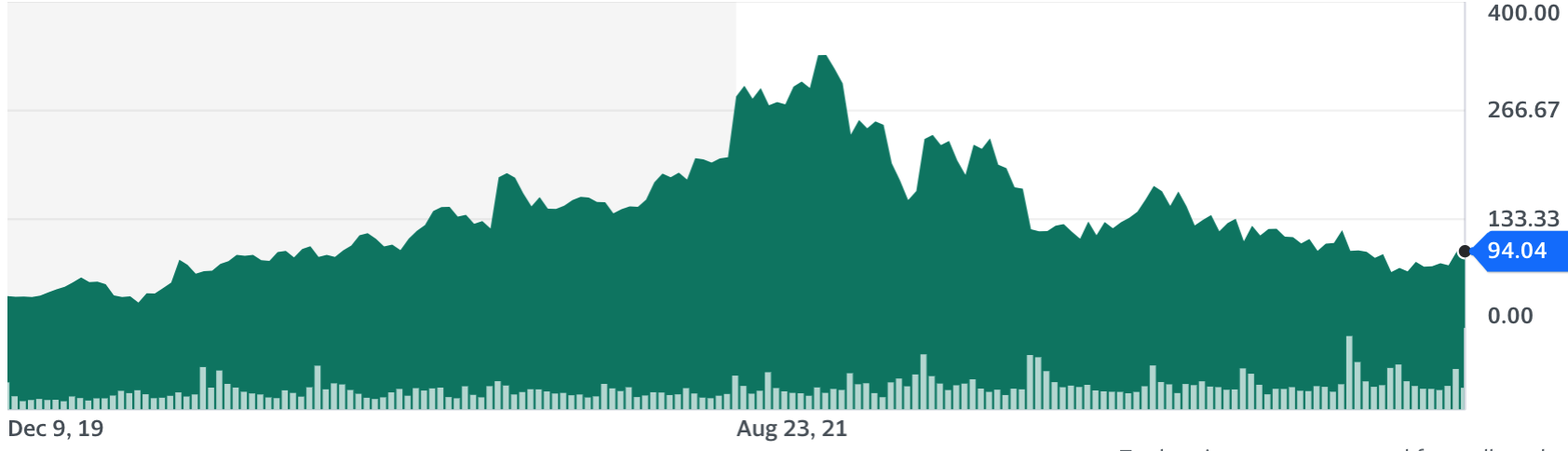

Bill Holdings (BILL: $94, up 22%)

High Technology Portfolio

Payments solutions company, Bill Holdings (new name) posted a monumental third quarter performance, with revenues at $270 million, up 63% YoY, compared to $170 million a year ago. The company posted a profit of $60 million, or $0.50 per share, against a loss of $9 million, or $0.08, with a phenomenal beat on consensus estimates on the top and bottom lines.

The company currently serves over 450,000 small businesses, up from 386,000 last year. It has processed payments of $65 billion across 21 million transactions, an increase of 13% and 36%, respectively. In addition to subscription and transaction fees, the company generated interest earnings of over $30 million on the customer balances that it holds on its books. (With the higher rates come some benefits!)

Bill and its subsidiaries Invoice2Go, Divvy, and Finmark offer small businesses with a seamless solution to handle all of their back-office operations. This includes accounts payables management, receivables, spend management, and everything in between. It currently counts over 6,000 accounting firms, including PWC and KPMG as its partners, along with 6 of the top 10 financial institutions.

Thus far, the company has barely scratched the surface of its massive global potential, which it estimates at 30 million small businesses and sole proprietorships within the US alone, and over 70 million around the world. It is currently a leading provider in this space, with features and functionality that are second to none, as evidenced by its phenomenal 130% net dollar-based retention rate, which means 30% of additional revenues coming from existing customers.

During the quarter, the company repurchased $27 million of stock, which we think is rather premature, but it is mostly aimed at making up for stock-based compensations to avoid the dilution of common shareholders, which is commendable. Given its robust balance sheet with $2.6 billion in cash, debt of $1.8 billion, and coupled with its newfound profitability and cash flow of $34 million, it will afford to reward shareholders generously. Watch for bigger buybacks and a dividend in the coming years. Our Target is $125 and our Sell Price is $80. This stock is a recent case of holding onto a stock that had gone below our Sell Price. In many cases, it is wise to hold on to these great companies.

-----------------------------------------------------------------------------

Moderna (MRNA: $137, up 3%)

Healthcare Portfolio

MRNA vaccine pioneer Moderna released its first quarter results last week, reporting $1.9 billion in revenues, down 70% YoY, compared to $6.1 billion a year ago. The company posted a profit of $80 million, or $0.19 per share, against $3.7 billion, or $8.58 per share. The stock soared following the results, owing to a stronger-than-expected, surprise profit, and the top-line performance during the quarter. The drop in the company’s sales was expected as the demand for its COVID-19 vaccine starts to wane, however, a sudden spike in demand for its only marketable product, gave investors much to cheer. Moderna maintains its guidance for 2023, with sales expected at $5 billion from advanced purchase agreements of the same Covid vaccine, around the world, throughout this year.

The company posted a profit during the quarter, after accounting for $150 million in write-offs for vaccines that exceeded their shelf lives, in addition to $135 million in unused manufacturing capacity expenses. It is further encouraging to see new contracts being inked for its COVID-19 vaccines across US government agencies, pharmacies, hospital chains, and more, pointing towards resilient demand even as the peak of the pandemic is past us.

Moderna expects the demand for boosters, especially among seniors and people with weak immune systems to continue, resulting in a steady revenue stream. The company currently has five different vaccines in early clinical trials and expects to launch its RSV* and flu vaccines in 2024. It projects revenues between $8 billion and $15 billion by 2027 from 6 major respiratory vaccines. The windfall gains during the course of Covid have helped the company double down on its R&D, with expenses in this segment up by 100% YoY. Moderna has used some of the proceeds of its huge inflow of revenue to reward shareholders, with $530 million in stock repurchases during the quarter. With $3.4 billion in cash and $1.8 billion in debt, it remains well-capitalized for the road ahead. As noted above Moderna has projected 2023 sales of the vaccine to reach at least $5 billion. That figure does not account for contracts that could be signed this year. The company specified the potential for deals with the U.S., Europe, and Japan, among others. The company will increase its R&D investment to $4.5 billion in 2022, it said. Moderna has 48 programs in development, with 36 clinical trials ongoing.

* Respiratory syncytial (sin-SISH-uhl) virus, or RSV, is a common respiratory virus that usually causes mild, cold-like symptoms. Most people recover in a week or two, but RSV can be serious, especially for infants and older adults.

Our Target is $250 and our Sell Price is $150. Yes, the stock is below our Sell Price so you should consider the risks here. We’re going to stick with it, as we see tremendous growth ahead as its R&D begins to pay off. Yet there are no guarantees, and sometimes Wall Street doesn’t enjoy the wait, punishing the stock along the way. It is currently out of favor, but we see it differently, and view it as a tremendous buying opportunity.

-----------------------------------------------------------------------------

Universal Display (OLED: $137, up 3%)

Special Opportunities Portfolio

A leading manufacturer and designer of energy-efficient displays and lighting technologies, Universal Display released its first quarter results last week, reporting $130 million in revenues, down 13% YoY, compared to $150 million a year ago. The company posted a profit of $40 million, or $0.83 per share, down from $50 million, or $1.05, owing to inflationary pressures and macro uncertainties.

The company generated $70 million in material sales during the quarter, down 20% YoY, compared to $87 million. This is followed by royalties and licensing fees at $55 million, down 8% YoY, compared to $60 million, and its up-and-coming contract research services business at $5 million, up 25% YoY, from $4 million. This segment is expected to grow exponentially as OLED technology gains pace.

While the company anticipates a slowdown during this year, largely owing to the macro uncertainties and inflationary pressures, it remains confident of steady tailwinds from a new OLED adoption cycle. It has since acquired the phosphorescent emitter patent portfolio of German-based Merck KGaA, in order to further strengthen its position in the segment, and capitalize on the broad secular tailwinds.

Universal Display disappointed investors with a bleak guidance for 2023, and during its first quarter results, it has continued to maintain the same figures, projecting a YoY decline of 7%. It has, however, signaled potential for a strong rebound in 2024, which has helped the stock command higher multiples, despite being one of the worst performers in the semiconductor segment over the past year.

This is a stock for the long-term, being steeped in science and deep research; investors won’t do well to judge it on its quarterly game. The stock has been on an uptrend throughout this year, posting gains of 28% YTD, but still remains down by over 45% from its peak in 2021. It issued a dividend representing an annualized yield of 1% (Zzzzz), before ending the quarter with $160 million in cash and just $40 million in debt. Our Target is $145 and the Sell Price is $115, which we are raising to $130. If it goes below this price, we are out. Having added it at $95 in 2018, it’s been a long haul here with a lot of disappointments. Yes, you’ve made money, but we are tired of the slowing growth of the company in a market where they should be growing at 20-30% a year. This is not happening. $130 and out.

-----------------------------------------------------------------------------

Teladoc Health (TDOC: $26, down 1%)

Early-Stage Portfolio

Telemedicine and virtual healthcare company Teladoc released its first quarter results recently, reporting $630 million in revenues, up 11% YoY, compared to $570 million a year ago. The company posted a loss of $70 million, or $0.42 per share. The results were ahead of estimates at the top and bottom lines. The company continued to see growth across key metrics and segments last quarter, starting with total integrated care members at 85 million, up from 79 million a year ago. The BetterHelp online mental health platform ended the quarter with 470,000 paying members, up from 380,000 users a year ago, followed by its chronic care program enrollment at 1 million users, up from 910,000 users during the year ago period.

Full-year revenue increased to $2.4 billion last year. Management expects revenues for 2023 to be about $2.6 billion, an improvement of 9% from 2022. Adjusted EBITDA is anticipated to be about $305 million, which suggests 24% growth from the 2022 figure of $245 million.

Teladoc, however, witnessed a marginal decline in its average revenue per user at $1.39, down sequentially, as well as on a YoY-basis, at $1.44 and $1.41, respectively. The company’s enterprise business that caters to employers and health plans reported $350 million in revenues, up 5% YoY, and represents a key growth driver for the company as employers revamp their health and wellness perks.

As demand for weight loss drugs continues to grow in the US, Teladoc’s pre-diabetes and weight management program is set to join the fray, offering diet and nutrition counseling, mental healthcare, fitness tips, and even prescriptions for GLP-1 drugs such as Ozempic. Following its fiery streak during the pandemic, Teladoc is set to play an outsized role in US healthcare, even though growth has flat-lined on a YoY basis.

As of now, the company remains focused on profitability, laying off 300 workers in January to lower operating costs, but its biggest expense still remains user acquisition, via extensive digital advertising spending. The stock trades at a valuation of just 2 times sales, with $900 million in cash, $1.6 billion in debt, and $230 million in cash flow. The big drag of course is profitability. Wall Street just can’t take it. And we don’t blame them (whoever “them” is. Oh – it’s us!) Yes, we can’t take it. What can one do about this is the question. You can sell all, buy more, or sit and wait. We remain quite amazed at the huge revenues that the firm has created, but we are also amazed at how they can’t figure out how to make money.

Our Target is $72, which is way too high. We’re lowering it to $42. We have no Sell Price currently because we can’t imagine the stock going much lower from here. But in reality, anything can happen on Wall Street. Thus, we are instituting a Sell Price at $22. $22 and out. The investment has certainly been a disaster as we are down significantly. This was one where we should have honored our initial Sell Price.

-----------------------------------------------------------------------------

The High-Yield Investor

The Bull Market Report

Jay Powell raised a few eyebrows this week saying that conditions in the banking industry are getting better when reportedly half of all banks are already “potentially” insolvent. Is he whistling in the dark, hoping we don’t panic and trigger a 2008-style crash? Has he gone crazy?

Despite all the anxiety and dread, we have to come down (a little narrowly) on his side. We’re actually a long way from a Lehman Brothers “too big to fail” failure. We know this because we know how the banking landscape has actually evolved in the last 15 years. There are 4,200 banks. Most are very small, not even “regional” in scope. At a glance, not 400 of them are big enough to be publicly traded and the bar there is extremely low. The smallest bank stock on our radar, Carver (CARV), is worth just $18 million. It’s hurting, don’t get us wrong. Earnings have crashed in the squeeze between higher lending rates and deteriorating credit quality. But it’s 0.02% the size of Citi (C) today. Its problems are not systemic or contagious. Ten years ago, the 10 biggest institutions held more than half of all U.S. deposits. Today their footprint has grown to two thirds of deposits, leaving everyone else fighting over a shrinking piece. That’s bad for all those smaller banks, but as long as the bulge bracket remains strong, the industry as a whole won’t show much strain.

And the Big Banks just reported earnings. They’re confident. They’re doing fine. While they are arguably too big to be allowed to fail at this point, they’re big enough to look out for themselves. That’s what Powell sees. While it’s sad and a little scary to see a Silicon Valley Bank or a First Republic Bank implode, these companies weren’t even 1/20 the size of Lehman Brothers back in the day. They make headlines but headlines don’t rock the boat. Remember, there are 4,200 of them and between them they hold a third of all U.S. deposits. Their feelings don't bend the fundamentals for the system as a whole.

If you're worried about the system as a whole, you should be worried about the fundamentals. Everything else is just feelings, and Wall Street has infamously never shown a lot of respect for emotion unless there are numbers to back it up. Will Powell keep tightening until a truly important institution breaks? That’s the real question because your gut response says a lot about your sense of the Fed’s authority. If you think Powell and company are more likely to overreach than correct at the first sign of crisis, you’re in a miserable situation. We can’t fight the Fed. If the Fed is incompetent, there’s no place to hide.

Lately the market’s faith in the Fed has been faltering. We started to see it when Powell suddenly decided in 2019 that there was no reason to maintain interest rate discipline in the absence of inflation. He was more interested in boosting the economy and keeping the market cheering. Then in the early stages of the pandemic, he clearly panicked. When the threat of a 2008-style credit crisis became real, rates went straight to zero. Now here we are. Powell is talking tough as long as inflation is on the table, but it’s hard to ignore his track record, and harder than it once was to trust the Fed to act as long-term steward of the economy as a whole.

We’re a long way from the invincible era of Alan Greenspan, much less Ben Bernanke. But even those icons ultimately revealed feet of clay. Greenspan triggered both the dotcom and the 2008 crashes. Bernanke cleaned up the latter, but the results were far from robust. At the end of the day, while we can’t fight the Fed, we’re still free to make up our own minds. We think Powell is right to do what it takes to beat inflation into submission. We also think he’s right that the banking environment as a whole remains robust.

But we know that if big banks start breaking, he’ll flinch. For now, we are not buying the little banks on the dip. We are actively culling our Financial recommendations instead. Let this shake out. We’ll be here to pick up the pieces, just like Jamie Dimon and his cronies at the big banks are picking them up even as we speak.

AGNC Investment (AGNC: $9.91, down 4%. Yield=15.2%)

High Yield Portfolio

CUTTING COVERAGE

One of the largest Mortgage REITs, AGNC Investment released its first quarter results two weeks ago. The company managed to deliver a profit of $410 million, or $0.70 per share, against $380 million, or $0.72 per share, but this came at the price of a massive miss on top-line figures. While the company’s agency mortgage-backed securities (MBS) portfolios started to perform well during the first half of the quarter, things started turning sour in the later weeks, with regional bank instability, interest rate volatility, and a broader macro uncertainty, all weighing it down. As a result, the company’s MBS portfolio underperformed treasuries and swaps in March, resulting in a negative economic return.

The negative economic return resulted in a $0.43 decrease in its book value to $9.41 per share, compared to $9.84 the prior quarter. As a result, the stock now trades at a premium to book value, making AGNC the only Mortgage REIT currently to do so. This is not consistent with the mood around this corner of the market, where stocks generally trade at significant discounts to book value because investors remain wary and reluctant to hold their positions in what could become an economic crisis. With that said, now is the perfect time to exit this stock, as it is unlikely to continue to trade at a premium forever.

It might seem crazy to exit this stock right now with the stock producing a 15% annualized yield in monthly $0.12 per-share installments. But we believe that its spread income has peaked and will start deteriorating from here. While remaining assets theoretically pay enough now to cover the dividend, AGNC has consistently sold off its holdings, down from $90 billion to $57 billion over the past two years, all the while continuing to dilute investors with fresh stock issuance, undoing any potential bright spots. We’ve collected a lot of money from dividends over the years, but the retraction in the stock itself has taken it all away. We reluctantly say goodbye to this Mortgage REIT. The inverted yield curve has taken another prisoner.

Apollo Commercial Real Estate Finance (ARI: $9.52, down 6%. Yield=14.7%)

High Yield Portfolio

This New York-based mREIT predominantly invests in senior mortgages, mezzanine loans and other real estate-backed debt instruments. Despite all the anxiety around the credit market, business is actually good here . . . and we have more than vague assurances to back up that statement. The latest quarterly revenue figures show $70 million coming in (up 29% compared to $55 million a year ago) and a full $0.48 per share turned into profit. A year ago, Apollo was running at full speed and only booked $0.35 per share in profit. That was enough to pay the long-established dividend and it's now likely that management will either stockpile the extra cash for any anticipated rough times ahead or, in the absence of real strain, simply distribute it to loyal shareholders.

The company ended the quarter with a loan portfolio worth $8.5 billion, with an unlevered, all-in yield of 8.6%. It funded an additional $170 million worth of loans, mostly refinancing two floating rate mortgage loans, in addition to the add-on fundings of $114 million during the quarter. The firm further received proceeds to the tune of $500 million from repayments and the sale of loan assets.

Originations have taken a plunge during the first quarter, largely a result of the high interest rates that have made it too expensive to borrow. The rising interest rates over the course of the past year and a half have served the firm well, since 99% of its portfolio remains concentrated in floating rate loans, but this creates a downside risk when the Federal Reserve changes course and starts lowering rates.