Bull Market Report Investor Notes: August 26, 2019

The Weekly Summary

The market recovery that started when calmer heads prevailed on Monday evaporated on Friday as comforting words from the Federal Reserve were unable to cut through new tariffs from China and tough talk from the White House. As we write this, it's looking like tomorrow will be another down day.

We've seen a lot worse. Admittedly, it's not fun to see what looked like a promising week slip away, leaving the S&P 500 and our recommendations down around 1.5%, with another 1% decline brewing overnight. However, as long as the economy remains relatively robust and corporate earnings hold up, there's no reason to get nervous.

The Fed is still our friend. The next interest rate cut may be only three weeks away. We also doubt that the market has had time to fully appreciate last month's rate cut just three weeks ago. Until that happens, the situation looks no worse than what we faced when summer 2018 came to an end.

Stocks are fairly valued relative to future growth prospects. Taxes are low. Expectations are realistic. And yes, the trade war continues. None of this is new. None of it has changed. The only thing that's changed is that investors and corporate executives alike are getting frustrated with a lack of clear guidance from Washington. Until we get clarity, stocks are stalled at least until the next earnings cycle starts in mid-October. We're willing to wait through a few stormy weeks to reap the rewards ahead.

There’s always a bull market here at The Bull Market Report! This week we're providing two separate "Big Picture" views, one tactical and one that's more strategic. The High Yield Investor reviews two of our most defensive recommendations if you're looking to pivot to the sidelines, but that's for subscribers only. Likewise, updates on our Stocks For Success (up an average of 103% since we started coverage, beating the S&P YTD by 10%) are behind the paywall. Want a free trial? Let us know!

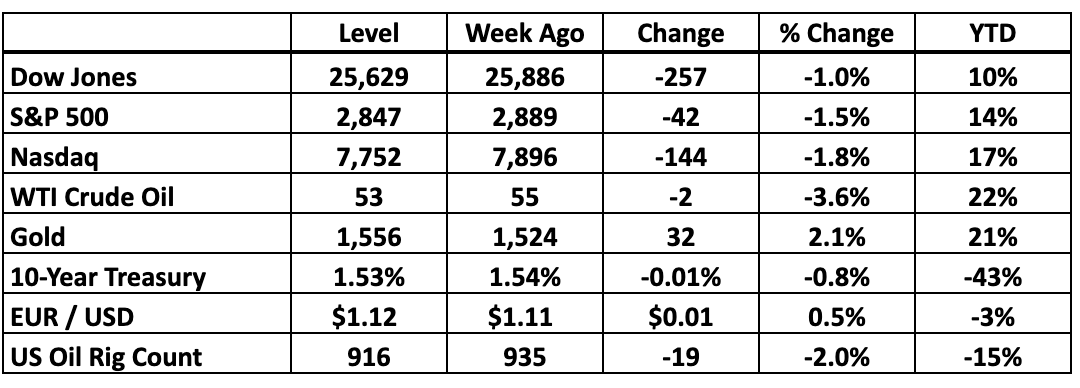

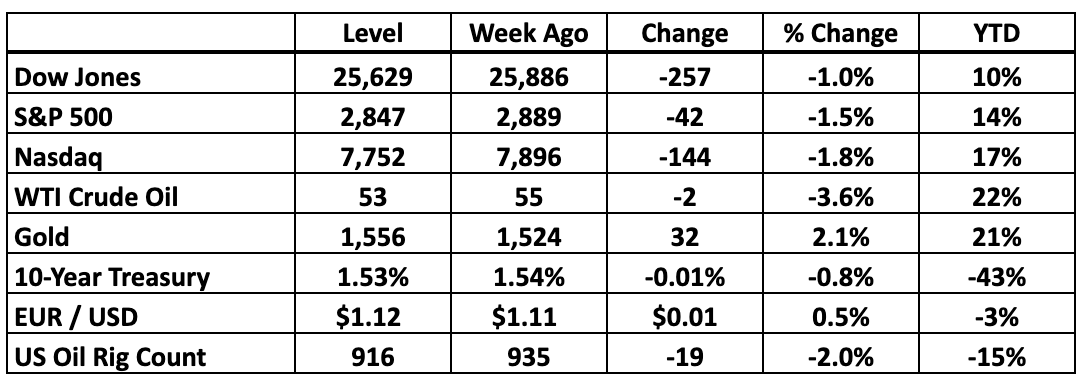

Key Market Indicators

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: Splunk's Acquisition Agitation

While most investors would be happy to see their chosen stocks keep making money forever, others get caught in a mindset where every consideration vanishes but the exit. These are the people who routinely sell Splunk (SPLK: $119, down 5% last week) every time a quarter goes by with no acquisition announcement. As far as they’re concerned, the company only exists to attract a lucrative offer from somebody bigger.

We question that logic because we know how the corporate consolidators actually think. When someone like Microsoft, PayPal or Salesforce.com pays a premium to absorb a smaller rival, valuation usually takes a back seat to strength. Dynamic companies with solid balance sheets, aggressive business plans and the growth trajectories to back them up are naturally more attractive than those facing resistance creating new markets or competing in established ones.

Good companies get taken out at a high price. Every day their management teams negotiate with potential suitors makes them more valuable and sweetens the ultimate offer. In the meantime, shareholders see the progress, giving the stock room to climb on its own. That’s what success looks like. Succeed long enough on your own and you find yourself in the consolidator’s role, buying small companies to bolt their capabilities onto what you already have.

That’s how the buyers keep growing. Splunk is at that stage now, which is in the background of its post-earnings swoon last week. Some people were really hoping that Salesforce.com would take it out. Maybe one of these days management will get an offer they truly can’t refuse.

In the meantime, we like our companies as going concerns. They’re attractive on their own and have a compelling business plan and the resources to achieve their potential. If someone wants to accelerate that glide path by paying a premium above the present value, we won’t complain . . . but if anything, it’s a little disappointing because it takes a great stock off the market. We’d rather have them stick around and keep making money year over year.

Splunk has made BMR subscribers about 45% a year for the last 3.5 years. Accepting a takeout offer, even if it’s in the $150 zone, ends that journey with one last exclamation point.

That said, deal activity is getting more intense and the price tag on each major acquisition is rising. People in the Technology sector in particular see bigger deals ahead. We might not see Splunk get bought out any time soon, but any of our Aggressive positions and most of our smaller High Technology stocks would make some consolidator a tempting prize.

Just look at Roku (ROKU: $138, up 5%). It’s come a long way for us in the last 14 months, but it’s still “only” a $16 billion company. Someone like Apple could pay cash once they get serious enough about controlling the burgeoning Streaming Video market. That day is coming. For now, we’re happy to let the stocks evolve on their own.

-----------------------------------------------------------------------------

The Bigger Picture: Far From The End Of The World

Wall Street has been an extremely bumpy ride this month, with the S&P 500 down 4% and the BMR universe dropping 3% since the trade war stole the spotlight from the most supportive Federal Reserve meeting in ages. And indications as we write this Sunday evening are for a big drop at the opening Monday. A little shell shock is natural. After all, it isn’t the end-to-end decline that hurts as much as the emotional impact of weeks of reversals and accumulated uncertainty.

We did the math and August is indeed shaping up as 25% more volatile than average, based on the way stocks have been swinging in the hours between the market open and the close. Normally we’d expect to see a 1.3% range from intraday low to the high. This month is tracking above 1.6%, which puts it on the edge of the top quartile in terms of volatility.

In other words, we should expect to see 3-4 months this wild every single year we’re in the market. Last year saw ambient volatility surpass what we’re seeing now in February, October and December. None of them were great months for investors, but they were all survivable. The world did not end.

Of course an uptick in volatility often takes stocks down, but the math at this point is far from apocalyptic. Normally the S&P 500 goes up seven months of the year and drops in the remaining five. The only suspense is which seasons will be the bullish ones and how large the moves will be in both directions.

However, when stocks are moving this fast during a typical day, the odds of a “good” month drop to about 50-50. Again, that’s far from an automatic loss, much less any kind of sell signal. It’s simply an expression of the statistical facts. When stocks are moving fast, volatility spikes. Any sudden lurch to the downside will generate wild intraday swings.

The open question is how long this choppy season lasts and how bad it gets. As a worst-case scenario, we went back to 2007-9, just in case you’re still wondering whether a similar recession is on the immediate horizon. Intraday volatility hit 1.8% in October 2007 when the market was in the earliest stages of deterioration, drifted in slightly elevated territory as the pressure built and then spiked with the Lehman Brothers collapse in September.

After that, it took another eight months for the wild swings to recede to normal levels. All in all, investors needed to hang on for a year and a half. If you’re concerned about a repeat of that cycle, we suggest making sure a combination of dividends and cash reserves will take you through that length of time while waiting for the market to recover from an especially nasty downswing. Bear markets of that scale only happen a few times per century of course and we’re only a decade out from the last one. But for those looking to cover themselves from the worst likely scenario, these are the numbers.

We’re a long way from a repeat of 2008. While it only took 60 days for the S&P 500 to slip into 10% correction territory, the 20% bear market threshold didn’t come for another six months. In most down cycles, that would be close to the end. That time around, volatility got extreme before the healing began.

Corrections happen. Even recessions are a natural part of every long-term investor’s life. But based on the last one, people who stayed liquid and resisted the urge to liquidate doubled their money in the decade that followed.

That’s a decent long-term return for a few months of patience. And of course all of this is purely to quantify the worst downswing in generations. We see no sign of the current shudder turning into anything like that storm.

After all, we expect at least 2-3 months like this in every 12-month period. Wall Street was probably overdue a little rain. Once the clouds clear, stocks still look like the best investments around. The fundamentals aren’t deteriorating precipitously the way they did in 2007. Until they do, it’s just a little sprinkle.

-----------------------------------------------------------------------------

Amazon (AMZN: $1,750, down 2% -- all returns are for the week)

Amazon may be up only 16% YTD, but it's been a wild ride. The stock is positioned to pop back into the $1,900-$2,000 range where it traded for most of the summer.

The 2Q19 numbers were mixed, with revenue jumping 20% YoY and 17% from 1Q19 to $63 billion, but EPS of $5.22 fell short of analyst estimates (consensus was $5.57). Management also lowered 3Q19 income to $2.1-$3.1 billion, lower than the $4.4 billion the market had been expecting. The company also posted the lowest quarterly net income in a year, with just $2.6 billion.

However, all of this is being driven by the $800 million the company is spending to upgrade its facilities in an effort to speed up delivery times. Faster delivery means more revenue and net income in the long run, so Amazon is willing to trade some short term pain for long term gain. (What else is new for this company!)

Jeff Bezos pointed out that free one-day delivery is now available to Prime Members on over 10 million items, and “we’re just getting started.” Plus, the company’s high margin Amazon Web Services grew 37% YoY to $8.4 billion. Yes, Microsoft is picking up steam in cloud computing (which we’ll get to in a moment), and that’s why AWS slipped from 41% YoY growth during 1Q19. But 37% is still astounding, and this is still by far the dominant market leader, so it’s worth focusing on the big picture here. Amazon may have lightly stumbled in this earnings call, but that’s only because its eyes are on the long-term prize. Don’t expect this gentle stumble to send the company reeling any time soon.

BMR Take: Amazon just opened its largest-ever campus in India, where the company is committing $5 billion to grow into that burgeoning market. The company is also growing out its Portland Tech hub, not to mention building its famous ‘HQ2’ in Virginia outside of Washington, DC. Plus, AmazonFresh – the company’s grocery delivery business – is expanding into secondary markets at the moment like Houston, Phoenix and Minneapolis. This plays into the faster delivery times initiative that Bezos and company have been laser-focused on. In short, Amazon isn’t done disrupting the world, in fact – to quote Bezos again: “We’re just getting started.”

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.