We all got to a week to brag about, with the S&P 500 and Dow industrials pushing through long-awaited milestones (3,000 and 27,000, respectively) and our universe keeping track with another 1.2% net gain. The broad market is finally catching up a little. They’re welcome to share the fun.

At this point the biggest threats to the rally revolve around investor nerve. After another year punctuated with harrowing slides and slightly slower recoveries, the index funds now have 8% to show for the trailing 12 months. That’s roughly what we expect from the market in a typical year. (Our active and closed positions have done a whole lot better in the aggregate, but you know how well you’re doing. If you’re disappointed, let us know. Write us at Info@BullMarket.com )

The danger is that investors simply won’t tolerate average historical returns in exchange for one of the most volatile rides in recent memory. Nerves are still a little frayed after last year’s slide took 20% away from portfolios between Labor Day and Christmas. However, in the absence of new fear factors, we suspect the mental bruises have healed and people are eager to get back to work accepting new records.

Yes, we’re finally back in full Bull Market mode after months of dithering over trade and Fed policy. Now it’s clear that the Fed isn’t going to keep fighting to preserve some abstract higher interest rate objective. Minimal inflation gives them room to take one of last year’s tightening moves away and leave us all with a reversion to more accommodative monetary policy in its place. And as for trade, a return to the status quo is evidently enough to earn applause. We know now what current tariffs mean for our companies. As long as the situation doesn’t degenerate, stocks now reflect all foreseeable downside.

Meanwhile, we’re three months closer to a resolution, whatever shape it takes. Corporate executives have had another quarter to pivot their supply relationships out of China into places like Korea, Japan, Taiwan and especially Vietnam, where we’re told the factories are full of U.S. products ready to ship to our stores free from tariffs. The Chinese domestic market hasn’t closed to our products. If anything, rolling back sanctions on Huawei should boost sales for U.S. Semiconductor manufacturer in the remainder of the year and beyond.

Earnings season starts this week with the first of the big Banks. From there, we’ll see hundreds of concrete examples of how well (or less likely, how badly) every company is bearing up under the current rate environment and trade regime. The rate environment is about to get better, starting with the Fed’s next meeting looming at the end of July. The trade regime has at least stabilized. What other risk factors can get in the way of the rally? We’re open to suggestions. If you’re nervous about anything, you know where to reach us.

There’s always a bull market here at The Bull Market Report! Our Earnings Previews start this week, which only subscribers get, but we're giving you a taste of our thoughts on Johnson & Johnson, which reports tomorrow. The Big Picture is all about the Fed.

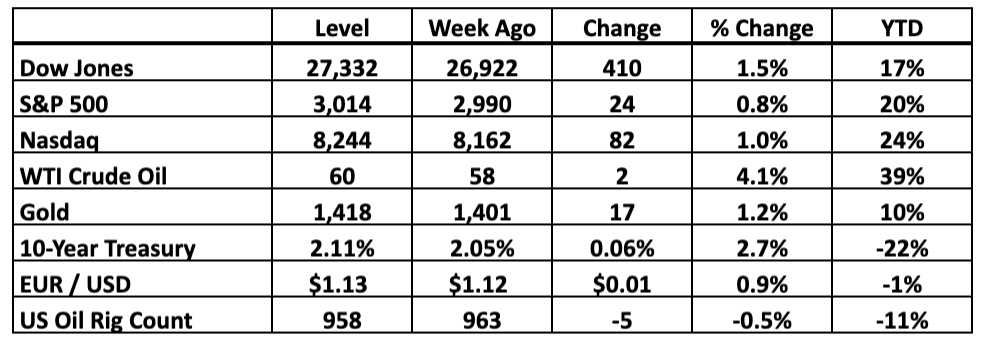

Key Market Measures (Friday’s Close)

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: Breathing Room For The Yield Curve

We’ve been fielding concerns about the Treasury yield curve since December, when middle-maturity government debt started to pay lower interest rates than shorter-dated counterparts. That’s an unusual situation because normally investors wait longer to get their money back, and naturally demand bigger yields.

The good news is that with the Federal Reserve likely to cut overnight lending rates in a few weeks, the curve is now unwinding what initially looked like an ominous recession pattern. While we’re still in an environment where 3-year Treasury yields are lower (1.81%) than 1-month bills (2.16%) and everything in between, at least the ends of the curve are moving in the right direction again now. A rate cut can make things better and relieve the recession pressure.

Back in March, most Treasury rates were clustered in an extremely tight band between 2.41% and 2.52%, with very little visible logic keeping the lowest rates on the short end and the highest ones reserved for longer-term debt. Investors got less from 5-year notes than 1-year bills, while 1-month bills paid more than 3-year notes. The most ominous thing of all was the extremely narrow spread between all of these maturities, hinting that the bond market had effectively given up on higher rates before 2026 at the earliest.

Since the Fed has historically needed to tighten as the economy expands, scenarios when rates have peaked generally point to a recession ahead. Similar yield curve inversions preceded all previous recessions in living memory, so this one gave the doomsday theorists plenty to talk about.

However, not every inversion foreshadows a recession, especially when the abnormal rate relationships only apply across part of the curve. This time around, the weight on investors’ minds was all about the dynamics of the curve itself and not the underlying economy. The Fed is tackling that confusion at the source.

Last year we heard persistent complaints that 3% is a hard ceiling for 10-year bond yields. Whenever long-term rates got that high for an extended period, stock investors got nervous and fled to the relative safety of bonds, pushing prices up and bringing the yields back down to “tolerable” levels.

(Remember, prices and yields always move in opposite directions, whether you’re dealing with Treasury bonds or our dividend-oriented recommendations. Buying low locks in a high effective return. Buying high locks in less real income.)

But while the far end of the yield curve became capped at 3%, the Fed kept pulling the near end up 0.25% per quarter throughout last year, compressing what was once 1.50% of room between the extremes to barely 0.48% today. After all, when the Fed makes overnight borrowing 0.25% more expensive, the rates on longer-dated loans need to go up too. That’s exactly what happened. Since the end of 2017, the Fed raised the overnight rate from 1.25% to 2.50% and 1-month Treasury yields moved up from 1.29% to peak at 2.51%.

Meanwhile, 10-year yields remained stalled at 3.0% and dipped to 2.0% when the market shuddered, forcing every point on the curve in between to flatten out or even drop below overnight rates. That’s just the return investors were willing to accept in exchange for relative safety. They weren’t looking for big interest. All they wanted was a secure place to park their funds.

Since the Fed acknowledged that it’s willing to not only “be patient” about future rate hikes but actively cut in order to keep the economy on track, the short end has plunged 0.35% to 2.16%, and a month from now it will be even lower. Longer-maturity bond rates have dropped too, but not as much. There’s now a fraction of a point more room between the extremes.

The curve is getting steeper again in the right direction, with the near end dropping and the far end staying roughly where it was. If 3.0% was the ceiling on the far side, evidently the only way to buy a little breathing space was to reduce pressure on shorter-term rates. That’s the only part the Fed controls, and it’s doing so now.

What this means for us is simple. First, as bond rates start declining again, investors need to look elsewhere to earn real income. That’s constructive for our High-Yield recommendations that pay a lot higher rates in exchange for what we consider only fractionally higher risk.

In general, lower bond yields support higher earnings multiples. Old-school valuation techniques suggest that a stock worth 13X earnings in a 3% world can go all the way to 20X when the Treasury market pays just 2%. We don’t anticipate huge moves from the Fed, but if you were worried about stocks getting frothy, the story is about to change.

And needless to say, cheaper money helps corporate executives dream a little bigger. They can fund larger and more transformative acquisitions or simply borrow enough to buy back more stock. Those with relatively weak balance sheets (we can’t think of any on the BMR list) get a second chance to clean things up before their debt starts choking them.

Throughout the process, consumers can keep spending without feeling the drag when the monthly bills come in. Lower rates are a boon for housing and auto markets. In a struggling economy, that’s the cushion that keeps the wheels turning. When the only apparent problems are tensions overseas and a persistent absence of inflation at home, the bulls get plenty of room to run.

Sooner or later recessions become inevitable. But with the Fed on the move, the yield curve now looks more like what we experienced in 1998 than any real pre-recession rate shock. Back then, Alan Greenspan jumped to correct a partial inversion in the face of tensions overseas. It took 33 months for the economy to contract. Investors who bailed out on stocks on the first glitch on the curve missed out on a 50% move higher and had plenty of time to reposition themselves when it was clear that the party was finally over.

The party’s not over yet. We might have years to let our winners ride. Either way, we’ll be watching . . . and the Fed is alert as well.

-----------------------------------------------------------------------------

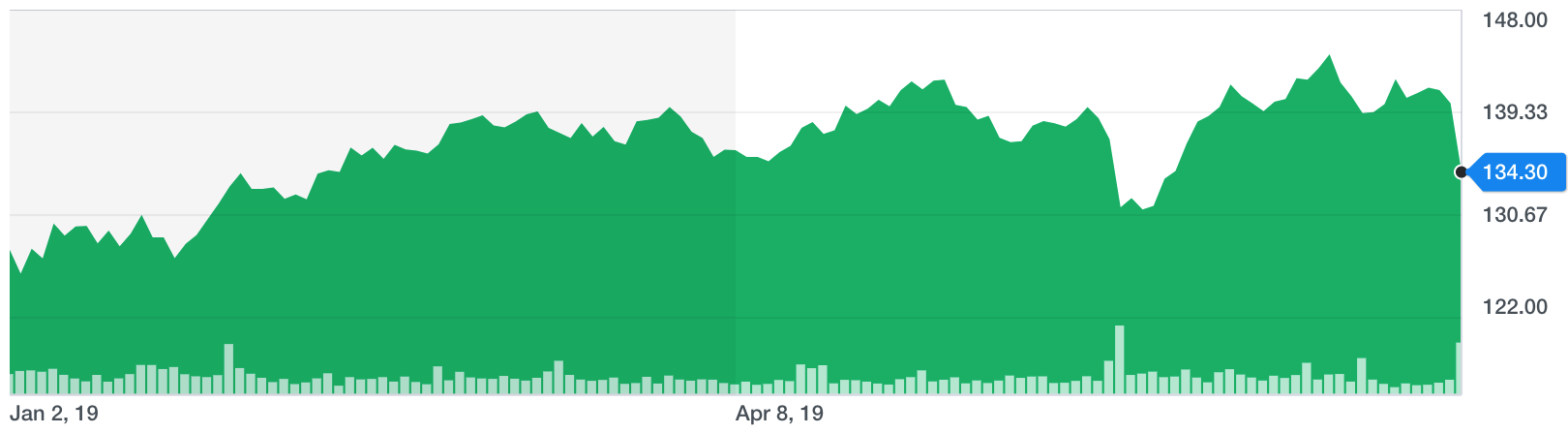

Earnings Preview: Johnson & Johnson (JNJ: $134, down 4%)

Earnings Date: Tuesday, 8:00 AM ET

Expectations: 2Q19

Revenue: $20.3 billion

Net Profit: $6.6 billion

EPS: $2.44

Year Ago Quarter Results

Revenue: $20.8 billion

Net Profit: $6.1 billion

EPS: $2.10

Implied Revenue Decline: 2%

Implied EPS Growth: 16%

Target: $150

Sell Price: We would not sell Johnson & Johnson.

Date Added: July 6, 2018

BMR Performance: 10%

Key Things To Watch For in the Quarter

Reports of a potential criminal investigation into the company’s talcum powder testing rocked the market on Friday, but we’ve seen similar headlines over the years and none of them have kept the company down for long. Even when judges have awarded massive damages to people who say they developed cancer after using Johnson powder, the judgments keep getting thrown out on appeal. The overhang just hasn’t turned into material financial liability yet.

Granted, legal costs have become a perpetual drag on Johnson & Johnson’s results, so we’ll be watching those figures Tuesday morning. Last quarter the company spent $400 million on lawyers. If that’s the status quo for the foreseeable future, the expense is built into the regular SEC statements now. Instead, we’re open to an upside surprise as management uses its $14 billion in cash (with another $4.5 billion coming in every quarter) to keep shareholders on deck.

The dividend has climbed to $0.95 per share, so short of a Boeing-style PR disaster we aren’t looking for a huge bump on the quarterly distribution here. However, buybacks are another story. We estimate that Johnson & Johnson has bought and retired 300 million shares over the past year, boosting its per-share earnings growth even as overall performance has been a little less impressive. There’s easily enough cash here to soak up another 200 million shares over the next 12 months.

But we’re not convinced Johnson & Johnson needs that much help in the long run. Sentiment may be skittish when the legal headlines get intense, but the fundamentals keep ticking forward, year after year. A slight revenue retreat this time around is all about the struggling Medical Device unit, which accounts for 30% of the company and keeps stealing focus from persistent growth from the much-better-performing Pharmaceutical operation. Factor out Medical Devices and the impact of a strong dollar and Johnson & Johnson is growing the top line about as fast as the market as a whole.

That’s all we really need this gigantic company to do. We’re here to capture that 2.8% yield while the giant keeps absorbing vibrant new Consumer and Medical brands and letting weaker operations go. The odds of that narrative adding up to big rewards over the long term are heavily weighted in our favor.

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.