by Scott Martin | Jul 8, 2019 | Free Newsletter (Sent Weekly Monday at 12pm)

When holidays break up the market week, a lot of investors simply check out until developments get more interesting. This was not one of those weeks. In the wake of an epochal Federal Reserve meeting and a make-or-break thaw on trade talks, nobody wanted to get trapped on the sidelines while all the fun was happening on Wall Street.

The S&P 500 is now not only breaking records on a regular basis but nudging toward the psychologically important 3,000-point line we suspected it could conquer before trade policy clouded the picture. The Nasdaq is back above 8,000 and even the rarefied Dow industrials, hamstrung by setbacks for many of its bellwether constituents, looks set to crack 27,000 for the first time in history.

As this past week demonstrates, investors have a right to be thrilled. BMR recommendations climbed 2.3%, eclipsing all the major indices as stocks on our list that once looked a little tired got a second wind.

With the exception of our most defensive Healthcare and High Yield portfolios, just about every major segment of the BMR universe beat the market. The core Stocks For Success group gained 3.0% and Technology jumped 3.4%, but even when you get down to the volatile Aggressive portfolio most of our names are in the money and ahead of the game.

We also got outside confirmation of that outperformance this week. First, our submission to this year’s MoneyShow Top Stock Picks competition did better than any of the other 100 participating market watchers put forward. Yes, we gave them Roku (ROKU: $98, up 8% this week), which has climbed so fast that we’re once again approaching triple-the-money returns there since 14 months ago when we added it, and we came out #1 in the competition! We still love this stock. It’s hard not to, when it’s up another 22% since the MoneyShow numbers were compiled at the end of June.

But victory is not just about one stock. Counting dividends, our active universe is up 35% YTD, which is great even by our standards. For comparison, the S&P 500 is up 19% over the same period and is in the throes of its biggest rally since 1997. However, in a year when only two mutual fund managers on prestigious lists scored even 3 percentage points better than we did, it’s nice to see that we’re not only delivering absolute numbers but staying far ahead of the pack.

In this position, our strategy revolves around expanding the lead and resisting the urge to change what clearly isn’t broken. Our recommendations are working. The ones that fizzled are gone, replaced with the most attractive stocks the market gives us in the present. As the economy shifts, we’ll shift with it. For now, no course correction is required.

Earnings are coming. The trade situation has stopped escalating to the downside. Everyone hopes the Fed will cut interest rates at the end of the month, especially after Friday’s unemployment number came in a little higher than expected. Jay Powell will give us some hints in his Congressional testimony later this week. And our companies are still racking up cash a lot faster than the market as a whole.

There’s always a bull market here at The Bull Market Report! The Big Picture takes advantage of the last lull before earnings season (our Previews start next week, which only subscribers get) and then it's good to check in on one of our biggest and steadiest stocks.

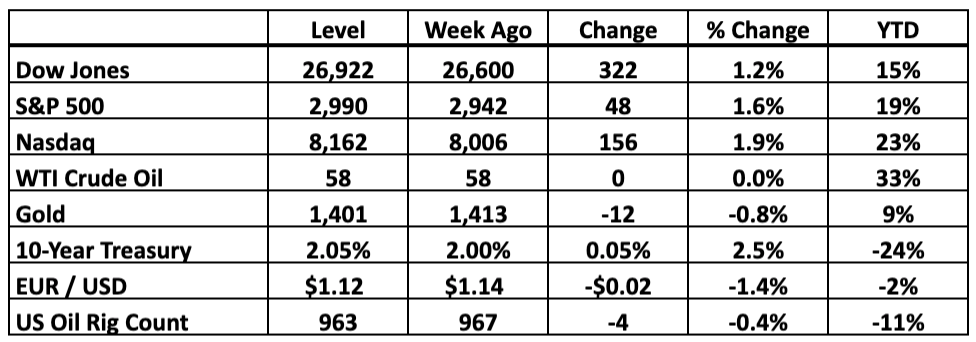

Key Market Measures (Friday’s Close)

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: Get Ahead Of The Earnings Crush

It happens every 90 days with the big Banks officially starting the 2Q19 earnings season. We’ll see this next Monday, which means this is the last Bull Market Report before the flow of Previews and Reviews starts up again next week. As such, we have an opening here to provide a few strategic notes that will apply throughout the cycle.

First, in terms of timing, you can expect our season to start relatively calmly with Johnson & Johnson the morning of July 16 followed fast by Netflix (NFLX: $381, up 4%), The Blackstone Group (BX: $47, up 6%) and mighty Microsoft (MSFT: $137, up 2%). Every one of them will go a long way toward setting the tone for the market as a whole to follow, with the Technology names likely to grab more than their share of headlines. We’ll say more about them all in the days leading up to their numbers.

The real fun starts the week after, when almost 25% of our recommendations that report quarterly results are on the calendar, and then we wrap up July with a surge of 20 BMR companies crowded into a five-day period. After that, the flow tapers down fast. While we’ll keep reading 10-Q filings through early September, they’ll be more about weighing stock-specific nuances than figuring out the broad strokes.

For us, the broad strokes will be in place after July 30 with numbers from Apple (AAPL: $204, up 3%). Three weeks from now, we’ll have a pretty good sense of how our entire universe did last quarter and the business conditions their management teams see ahead. From there, we can extrapolate most of what’s going on elsewhere and then, if the numbers are as good as we expect, we’ll have 10 weeks to ride the wave.

That’s what every earnings season is all about. The day the 10-Q gets filed, we have absolute certainty on how well the company did in the trailing period. When our projections deviate from that reality, we adjust, and when that revised outlook changes investors’ sense of what the company is worth, the stock goes up or down in response.

But then the quarterly clock starts ticking again. The farther from that moment of 10-Q clarity we are, the more room Wall Street’s targets get to drift away from corporate reality. Eventually that drift reaches the point of maximum uncertainty and investors are more likely than ever to miss crucial clues that can sink or surge the stock.

We prefer to get most of our uncertainty out of the way as early in the cycle as we can. That way, we know what’s going on inside our stocks before other investors figure it out. If we need to raise our Targets or pivot out of a stock that’s finally hit a cash flow wall, we can do it while Wall Street is still off balance and under a cloud of suspense. And the market’s map of the new quarter’s winners fills in, we’re in a better position to make the first moves.

A few weeks from now, we’ll know which moves (if any) to make. For now, we already recommend all the stocks we can’t resist. There isn’t a lot of sizzle out there that isn’t already in the BMR portfolios. The market as a whole is still looking at 2% earnings deterioration this quarter, with growth not coming back until the end of the year. The BMR universe, on the other hand, remains on track to deliver 3% growth.

Our earnings targets have actually come up a little over the last three months. Despite all the noise distracting Wall Street since April, the signal is brighter than ever. Remember, most of our stocks have nothing to do with China. And they’re expanding sales fast enough to fight rising labor costs and other pressures on the bottom line. We’re in the hot spots. As they demonstrate that heat over the next few weeks, it’s likely that other investors will start jumping to our end of the market instead of the other way around.

-----------------------------------------------------------------------------

Johnson & Johnson (JNJ: $141, up 1%)

Aside from being an industry Blue Chip, this is one of the most dependable companies in existence – one of only two companies with a AAA credit rating (the other is Microsoft, another BMR pick). For reference, the United States government has a AA+ rating, so Johnson & Johnson is actually more creditworthy than the federal government.

J&J is a truly diversified Healthcare company, with a major Pharma presence. The company has a strong pipeline of drugs, with the FDA’s recent approval of Darzalex in combination with a Celgene drug for multiple myeloma patients adding another potential large revenue driver. Darzalex is already a blockbuster drug ($2 billion in sales last year), and now it can expand its market share (experts are predicting as much as $3 billion in revenue for 2019).

On top of that, the company announced plans for a Drazalex follow-up by partnering with Genmab (whom they partnered with on Darzalex) to create Hexabody-CD38. The beauty of the deal is Genmab will spend the upfront time and resources to prove that Hexabody has market potential, and only then will Johnson & Johnson decide whether to license the product. Thus there is limited downside here for J&J, and the company could land yet another multiple myeloma blockbuster like Darzalex.

The 1Q19 numbers were just okay, with U.S. sales up 2% YoY to $10 billion, while international sales fell 2% to $10 billion. The $20 billion in revenue per quarter has remained steady throughout the year, and illustrates just how consistent and dependable J&J is. With a $370 billion market cap in the Healthcare space, we’re not looking for massive growth here, just safe, consistent performance.

BMR Take: The stock is up 10% YTD, and the dividend of 2.7% is one of the most bankable in existence. That’s important given the overall market volatility. Remember, Healthcare is a defensive sector that’s primed to outperform during market downturns. Right now though, we’re looking at slow and steady growth for J&J, which is exactly what we expect. This is one of the few companies we would not sell here at BMR.

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.

by Scott Martin | Jul 1, 2019 | Free Newsletter (Sent Weekly Monday at 12pm)

Wall Street kept its fireworks in reserve last week ahead of a G-20 Summit that some predicted would either set the stage for a massive breakthrough on global trade or trigger a complete breakdown. We suspected that both extreme outcomes were unlikely when Chinese and U.S. diplomats are still so far apart on a negotiating framework much less the details that will make or break any proposed deal.

What we got was a continued truce in the trade war that will probably maintain the fragile status quo for months if not through the end of the year. That’s far from the worst scenario.

After all, the S&P 500 managed to rally 18% over the last six months, despite all the back-and-forth rhetorical escalation overseas and stalled earnings growth. We evidently aren’t alone in looking beyond the chatter to better days ahead, and with BMR stocks soaring 32% over the same period, it’s no wonder we’re optimistic.

However, success depends on your time horizon. While the last six months have been good for the market and our recommendations, this year-to-date rally needs to be weighed against an equally harrowing 4Q18 slide. Over the last 12 months, the S&P 500 is up only 8%. After that, while the market keeps tiptoeing from record to record, the gains have been grudging. Someone who bought the index in mid-September would be effectively back at zero now, nearly 10 months later.

BMR stocks, meanwhile, are up 40% end to end. Of course we weren’t in all of our current positions 12 months ago, so the raw number is a little misleading. We recommended 16 new companies over the past year and found compelling reasons to cut coverage on 7 others, keeping our portfolios fully exposed to the hottest areas of the market we can find. Some of those new stocks matured fast with 80-90% YTD performance. Others are taking a slightly slower route or are here to play a more defensive role, quietly accumulating dividends while flashier positions do their work.

All in all, however, our universe outperformed the index on the upside and held up a little better on the downside, both YTD and across the trailing year. BMR stocks held onto an 8% gain through the frustrating second half of 2018, then delivered nearly double what the market as a whole earned on the rebound. While nobody can say with certainty where we go from here, there’s no reason to assume that our track record will come to a sudden end now.

For one thing, BMR stocks collectively still have earnings growth on their side even though fundamentals for the S&P 500 now look stagnant (at best) through at least the release of 4Q19 numbers early next year. The trade war is only an intermittent threat where our recommendations are concerned.

And if the trade war becomes too big a drag on the global economy, the Federal Reserve has all but promised that it’s ready to cut interest rates. In that scenario, the tide of easier money helps all companies, and since ours aren’t under any pressure, the BMR universe stands to enjoy all of the benefits without accepting much of the trade war pain.

In the meantime, earnings season starts in a few weeks, so it’s time to start preparing for that cycle of corporate confessions. Expectations are low. A lot of investors have already discounted the entire earnings season and are looking toward the next Fed meeting at the end of July for a sign that it’s time to set off fireworks.

Remember, people who “sold in May and went away” last summer missed most of the year’s real gains, then buying back in when September rolled around only compounded their mistake. Summer can be a great time for investors, and at this point any significant progress on either earnings or trade will be enough to get stocks rallying in relief.

There’s always a bull market here at The Bull Market Report! The end of the quarter is the perfect time to review our strategic dividend focus in The Big Picture and then follow up with specifics in The High Yield Investor, which only subscribers got.

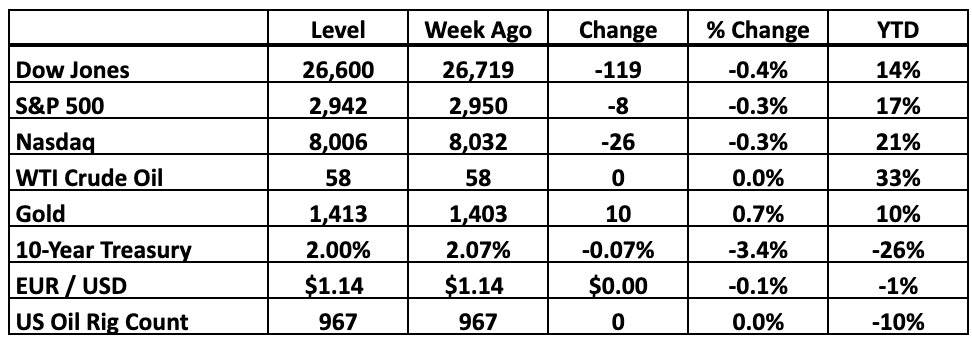

Key Market Measures (Friday’s Close)

-----------------------------------------------------------------------------

BMR Companies and Commentary

The Big Picture: Yield Is The Base

When stocks are soaring, our primary objective is to ensure that BMR subscribers are participating in the fun and not simply watching from the sidelines. And likewise, we urge you to buy the dips when a faltering market mood temporarily takes the stocks we recommend down with it.

Either way, we know the future will ultimately be better than the past. The only question is how fast we’ll get there in any particular swing of the market pendulum, given the bumps and detours that can make passive index fund investors so frustrated when the gains slow to a stall. The S&P 500 hasn’t even delivered 1% since mid-September while exposing shareholders to an extremely bumpy ride along the way.

Sometimes it isn’t worth the ride. In these consolidation periods when stocks have already burned through a lot of their rally fuel, the immediate returns have a hard time keeping up with the drain on investors’ nerves. That’s when we tend to spotlight our High Yield and REIT recommendations as an alternative to what could become months of empty angst.

Admittedly, these stocks and Closed End Funds aren’t risk free, but they pay back enough cash to buffer a lot of sluggish seasons. Right now someone could buy 10 shares of each of our 16 recommendations in these two portfolios for about $14,700. A year from now, the market may be willing to pay more or less to take those shares back from you, but along the way you’ll get 7% of that capital back in the form of dividends.

The question for you then boils down to where you think stocks will go in that year. Obviously our more aggressive, Technology-oriented posture has done a whole lot better than 7% over the past year, giving the active BMR universe a healthy 28% win in a period when the S&P 500 is only a little better than breakeven. But where will the next 12 months take us?

We’re optimistic that BMR stocks that led the world over the last year have what it takes to keep rallying as we look beyond 2019 into 2020. After all, 28% is a high enough score to justify a few rollercoaster lurches along the way. However, if the market as a whole suffers a sudden shock, the coming year could be a sour one for our universe as well as the S&P 500.

In that scenario, 7% looks pretty good. Depending on your situation, it could be enough to pay a few bills or provide the dry powder to buy temporarily depressed stocks on the dip. Either way, it’s a whole lot better than nothing, and it dramatically reduces the odds that you’ll need to liquidate at the bottom in order to raise cash.

And 7% isn’t even all that bad in absolute terms. Risk and returns go together. Treasury bonds are as risk-free as it gets, but the market won’t let you lock in more than 2% right now and that’s barely enough to keep up with inflation as it is. Stocks can soar or go over a cliff that takes them months or even years to climb back from, forcing investors to wait a long time before they get their money back.

The S&P 500 generally delivers somewhere between a 10% loss and a 20% gain across a typical 12-month period. Locking in a high dividend yield raises the floor and sacrifices a little absolute upside, smoothing the year-to-year return. In the past year, for example, our High Yield recommendations appreciated 3% beyond the dividends we got, translating into 10% performance for the group. Our REITs, on the other hand, are more about market performance, so we actually lagged the S&P 500 there over the past 12 months after factoring in dividend payments.

It happens. Next year these portfolio dynamics may reverse as the Fed pivots from tightening to a more relaxed policy and REITs go back on the offensive. As the market mood swings, we might see a prolonged stock slump crowd big money into both asset classes, adding significant appreciation to the 7% overall income base across the board. In a “flight to safety,” this is where nervous investors will come to hide. We won’t mind. We’re already here.

Either way, it’s all about diversification. We monitor every recommendation to ensure that they’re more likely to make their regular payments than their peers, but we also recognize that our view is always going to be imperfect. Sometimes one of our companies cuts its dividend after years of reliable performance and we need to evaluate whether it’s time to go. Because it happens so rarely, there’s safety in numbers . . . even if three of our sixteen yield choices cancel their distributions entirely, the aggregate performance floor for the group only drops from 7% to 5.5%.

We are confident that our dividend stocks will get through the next 12 months in better shape than that, in which case the real question turns back to whether you think you can do better than that income floor elsewhere. The S&P 500 may have what it takes. Year to date, the index is beating our REITs by 10% and is narrowly ahead of our High Yield portfolio as well. Our non-yielding growth stocks have rallied 40% in the last six months, so that’s an even better choice.

But if you think there’s even a chance that the coming year bodes badly for the market, it’s worth buying a little insurance that will enable you to squeeze at least some profit out of the seasons ahead. That’s what our yield portfolios are for. When our other stocks are making a lot of money, these quieter recommendations make a little money too. And when the market as a whole loses money, the dividends keep coming.

-----------------------------------------------------------------------------

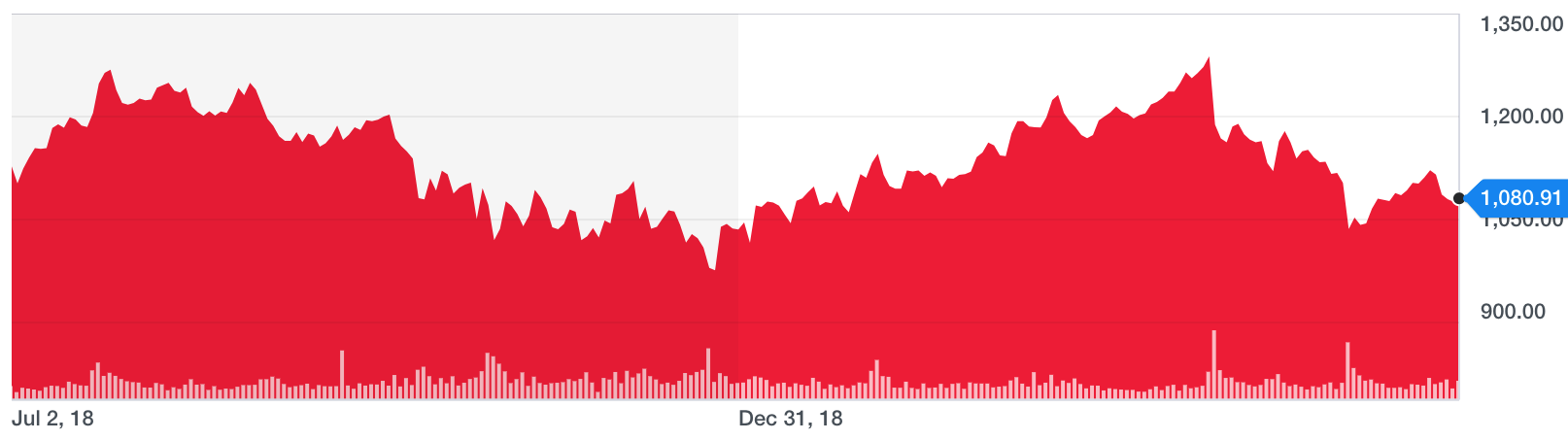

Alphabet (GOOG: $1,081, down 4% -- all returns are for the week)

Continuing with our Stocks for Success coverage this week, Alphabet hasn’t been as successful as we’d like (up 3% YTD), but that includes the May dip, which the stock has yet to recover from. We were looking at a 22% YTD return prior to the selloff and continue to believe the stock is a prime buying opportunity as this is one of the most bankable long-term investments in the world.

Alphabet has a lot going for it beyond a monopoly on Search. The company is introducing a video game streaming service called Stadia, which could disrupt the entire gaming industry the way Netflix disrupted Hollywood. Stadia will allow users to play games without the need for a console. Additionally, Alphabet is already testing its Project Soli technology, which allows users to operate smart devices with mere hand gestures (no more tapping or swiping). This has immense implications for the smartphone, tablet and even the burgeoning smart-watch industries.

On the financial front, Alphabet has grown revenue at least 20% per year over the last three years, but in 1Q19 revenue growth came in at 17%. That, coupled with macroeconomic concerns is what tanked the stock. Of course, the market is being hyper-reactionary. 17% growth for a $750 billion company is astounding.

And the deceleration is a blip, not a trend. With YouTube dominating in mobile video streaming (37% market share – next biggest players are Facebook and Snapchat with just over 8%), autonomous vehicle manufacturer Waymo coming online soon, and the aforementioned Stadia and Project Soli set to disrupt major industries, there are simply too many revenue drivers for growth not to spike back up over that 20% mark. Additionally, Alphabet is trading at 5.5x price/sales, and its five-year average is 6.5x. So the stock is less expensive along that metric.

BMR Take: With $115 billion in cash and only $12 billion in debt, Alphabet can afford to get creative moving forward. Of course, management already has so many innovative technologies on the horizon, it might be best to just wait and see which ones live up to – or even exceed – expectations. This is a company that’s so cutting edge Hollywood made a movie about two guys trying to get a job there (The Internship.) Revenue growth will pick back up in no time, and so will the stock. We’re reiterating our $1,450 price target and our ‘would not sell’ position.

NOTE: In our weekly paid subscription Newsletter, we do between 5 and 7 SnapShots and also support regular Research Reports. The last three stocks we recommended are already up 5% apiece. Plus, we have the Weekly High Yield Investor, whereby we discuss the 17 stocks in our High Yield and REIT Portfolios.

And to top it all off, we send News Flashes each day during the week. Got a question about any stock on the market? We'll answer. So if your favorite stock reports earnings or there is significant news, you will hear about it here first. If you want the whole picture, join the thousands of Bull Market Report readers who are making money in the stock market and subscribe here:

www.BullMarket.com/subscription

It’s only $249 a year, and later this year we will be raising it to $499 or even $999 a year, it is just THAT valuable. But we will lock you in for life at this lower price.

Good Investing,

Todd Shaver, Founder and CEO

The Bull Market Report

Since 1998

Subscribe HERE:

www.BullMarket.com/subscription

Just $249 a year, soon to go up to $499. But you are guaranteed the SAME PRICE forever.