by Todd Shaver | Nov 10, 2023 | Instant News Flash

Twilio (TWLO: $56) released its third-quarter results on Wednesday, reporting $1.03 billion in revenues, up barely 5% compared to $980 million a year ago. The company posted a profit of $110 million, against a loss of $50 million, or $0.29, with a beat on estimates at the top and bottom lines, coupled with a raise in the full-year guidance leading the stock to rally following the results.

The company has continued its streak of steady customer acquisitions, now serving 306,000 active accounts, up from 280,000 a year ago. Twilio, however, experienced a significant trough in its net dollar-based expansion rate at 101%, down from 122% last year. This can mostly be attributed to higher contraction and churn in its customer data platform, Segment, which it acquired a few years ago, coupled with slower growth across its other products.

Twilio is a cloud communications platform that enables businesses to build and deliver customer engagement experiences across multiple channels, including voice, text, chat, and video. Its platform is highly flexible and scalable, making it easy for businesses of all sizes to get started and grow. Its business model is based on a subscription fee for access to its platform and APIs. Twilio charges businesses based on the number of messages, calls, and other communications they send and receive through its platform.

Twilio's platform is easy to use, even for businesses with no prior experience with cloud communications, and it provides a variety of resources and support to help businesses get started and use its platform effectively.

Twilio integrates deeply with other popular cloud platforms, such as Salesforce, Shopify, and Amazon Web Services. This makes it easy for businesses to build end-to-end customer engagement solutions that leverage the best-of-breed technologies. The company offers several AI-powered features that help businesses automate and personalize their communication experiences. For example, its Predictive Dialer can automatically dial leads based on their likelihood of converting, and Twilio's Voice Intelligence can transcribe and analyze phone calls for insights. The platform is available in over 180 countries, giving businesses the ability to reach their customers wherever they are.

Twilio had a number of sizable new customer acquisitions during the quarter, which included a leading Latin American eCommerce platform, one of the largest North American financial services companies, and more. The company further signed a landmark agreement with Softbank, which will now be offering Twilio’s services through its channels for the Japanese market, helping its foray into Southeast Asia.

Investors appreciate the remarkable synergies that the company’s products, platforms, and copious amounts of user data are helping create. This makes Twilio’s efforts in generative AI and machine learning all the more meaningful, creating substantial moats against competitive forces going forward, all the while helping enterprise customers drive efficiencies and cost savings.

The stock is up 14% YTD but is still down dramatically since its peak in 2021, and as such it now trades at a little over 2 times sales. In addition to this, Twilio has over 30% net cash, meaning that its cash reserves at $3.9 billion, make up a significant portion of its market cap of $10 billion. The company is using this to repurchase stock with $1 billion in authorizations, having just $1.2 billion in debt, and $130 million in cash flow.

We would like to see revenue growth move higher in this coming year, as the company has a history of strong revenue growth. The last four years were $1.1 billion, $1.8 billion, $2.8 billion, and $3.8 billion. But 2023 is looking to hit just $4.1 billion. The company is now profitable, after years of waiting, which we are quite pleased about. And that bottom line trend is what Wall Street cares about now and it's ramping up fast. Consensus is looking for 30% earnings growth next year. Admittedly, we're here for the historical hypergrowth revenue narrative, so if sales don’t pick up, we will have to consider moving on to something more exciting. It could happen. Quite a few people think sales will hit $4.6 billion next year, which gets the engine humming again.

For now, our Target remains $135 and the stock is below our Sell Price of $65. In light of the revenue slowdown, we have to lower our Target to $80 and we are going to set a hard stop at $53 where it was last week. If it moves back down, we will have to let this wonderful company go. We added it at $52 in 2016 and watched it shoot higher to $400 two summers ago. It will hit that level again some day . . . but the slower sales growth gets, the longer that scenario will need to play out.

by Todd Shaver | Oct 31, 2023 | Instant News Flash

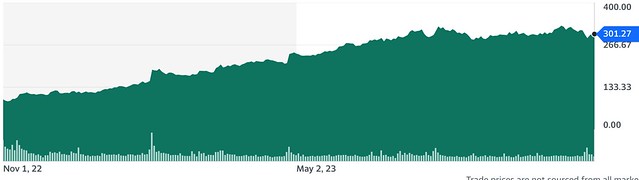

Meta Platforms (META: $301), the company behind Facebook, WhatsApp, and Instagram, released its third quarter results last week. It posted $34.1 billion in revenues, UP 23% YOY, compared to $27.7 billion, with a profit of $11.6 billion, or $4.39 per share, up by a mammoth 164%, compared to $4.4 billion, or $1.64, with a beat on consensus estimates for the coming quarter on the top and bottom lines.

Other key figures and metrics were just as exemplary, with daily active users across its family of apps at 3.14 billion, and monthly active users nearing 4 billion, both up by 7% YoY. Ad impressions across its platforms increased by 31% YoY, making up for the 6% decline in the average price of its ad inventory. All in all, this was a BLOCKBUSTER of a quarter for the company.

The company is fighting some growing legal, regulatory, and reputational risks. To start with, attorney generals from across the country have filed lawsuits against Meta for its addictive features, and 33 US states are now suing the tech giant for collecting data from young users without parental consent. Meta has always been mired with legal issues, ranging from antitrust to Congressional Hearings pertaining to political advertising and targeting. Time and time again, it has managed to rise above it all, with often nothing more than a slap on the wrist. So, we see no reason why it would be any different this time around, making this muted reaction nothing more than a minor overreaction.

In other news, the company is going all-out in pursuit of the Metaverse, now in partnership with Ray-Ban, and more realistic visuals. This is infinitely better than the earlier version, where people in the Metaverse resembled Sims characters. The new Metaverse looks ready to take on the likes of Zoom and Microsoft Teams when it comes to communications, making it an absolute game changer.

Following extensive cost-cutting measures, which involved laying off 24% of its workforce, Meta is now a lean, mean fighting machine. The stock is up by a stellar 140% YTD, and still remains off by about 22% from its all-time high of $384 set in 2021. The company is a cash machine, which helps support its generous $3.7 billion in repurchases, further aided by its $61 billion in cash reserves, $37 billion in debt, and $66 billion in cash flow. Our Target is $350 and we would never sell Meta Platforms. If revenues and earnings continue at this pace in the 4th quarter, and given a solid stock market, we can see that we might have a problem with the Target. We’d just have to raise it to $425.

by Todd Shaver | Oct 30, 2023 | Instant News Flash

Leading manufacturer of continuous glucose monitoring systems, Dexcom (DXCM: $88), released its third quarter results last week, reporting $975 million in revenues, up 27% YoY, compared to $770 million a year ago. The company posted a profit of $200 million, or $0.50 per share, against $110 million, or $0.28, with the spectacular beat on consensus estimates for the coming quarter leading the stock to pop 10% to $89 following the results.

In addition, the company raised its guidance for the full year, now expecting revenues between $3.57 and $3.60 billion, with a YoY growth rate of 24%. These figures can largely be attributed to the rollout of its G7 device, which saw quick traction owing to the company’s solid base of over 18,000 physicians already writing scripts for its products, along with the brand it has painstakingly built over the years.

Another key catalyst for the company was realized in recent months with Medicare coverage for its continuous glucose monitoring devices going live for people with Type 2 diabetes using basal insulin only. It also includes certain non-insulin individuals with hypoglycemia, bringing its total potential customer base within the US alone to about 7 million people, with the figure only set to rise from here.

Dexcom saw similar dynamics play out across various international markets, particularly in France, where Dexcom One has secured reimbursement for all patients on intensive insulin therapy. In addition, the company witnessed a sizable uptick in sales from Japan, which was the first to establish broad reimbursement for diabetics late last year, representing over 1 million patients.

Dexcom is a medical technology company that develops and manufactures continuous glucose monitoring (CGM) systems. CGM systems provide people with diabetes with real-time information about their blood glucose levels, which can help them to better manage their diabetes. Dexcom's CGM systems are used by over a million people worldwide.

Dexcom is well-positioned for growth in 2024 and beyond. The company has a number of new products and ideas in the pipeline that could propel the stock higher. Here are a few examples:

- G7 CGM system: The G7 CGM system is Dexcom's next-generation CGM system. It is smaller, more accurate, and easier to use than Dexcom's previous CGM systems. The G7 CGM system is expected to be launched in the United States in early 2024.

- Dexcom ONE CGM system: The Dexcom ONE CGM system is a lower-cost CGM system that is designed to make CGM more accessible to people with diabetes. The Dexcom ONE CGM system is expected to be launched in the United States in mid-2024.

- Implantable CGM sensor: Dexcom is developing an implantable CGM sensor that would eliminate the need for people with diabetes to wear a patch on their skin. The implantable CGM sensor is expected to be launched in the United States in 2025.

- CGM integration with other devices: Dexcom is working to integrate its CGM systems with other devices, such as insulin pumps and smartwatches. This integration would allow people with diabetes to manage their diabetes more easily and effectively.

In addition to these new products and ideas, Dexcom is also benefiting from a number of other factors, including:

- Growing demand for CGM systems: The demand for CGM systems is growing rapidly as more and more people with diabetes recognize the benefits of CGM.

- Expanding reimbursement coverage: More and more insurance companies are reimbursing for CGM systems, which is making CGM more affordable for people with diabetes.

- International expansion: Dexcom is expanding its international presence, which is opening up new markets for the company's CGM systems.

The stock is down 21% YTD but has been on an ascendant streak over the past three weeks after hitting the 52-week low of $75 on October 12th. Another great piece of news for investors is the announcement of a $500 repurchase program, creating additional support for the stock while rewarding shareholders generously, made possible by over $3.2 billion in cash reserves. The company has $2.7 billion in debt and $750 million in cash flow. Our Target remains $120 with a Sell Price of $81. This is no small company, clocking in with a market cap of $34 billion.

by Todd Shaver | Oct 19, 2023 | Instant News Flash, Uncategorized

Streaming giant Netflix (NFLX: $403, up $57, up 16%) posted a remarkable third quarter performance last night, reporting $8.5 billion in revenues, up 7% YoY, compared to $7.9 billion a year ago. The company posted a profit of $1.7 billion, or $3.73 per share, against $1.4 billion, or $3.10, in addition to a beat on estimates at the top and bottom lines, resulting in a strong 14% post-market rally in the stock following the results.

During the quarter, the company posted strong metrics across the board, starting with its new paid subscribers at 9 million, bringing its total to 250 million. This is largely the result of its crackdown on account sharing, which is now in full swing. Netflix has further rolled out its $6.99 ad-supported pricing tier in select regions worldwide, where these plans now account for over 30% of new subscriber additions.

In addition to this, the platform’s engagement metrics so far this year are off the charts. According to Nielsen, Netflix hosted the most-watched original series for 37 of the 38 weeks this year, and the most-watched movie for 31 out of the 38. Its share of total TV screen time within the US now stands at 8%, far ahead of other competitors, and only lagging behind YouTube, which has taken a slight lead at 9%.

With the success of content such as One Piece, The Witcher, and Top Boy, Netflix has officially cracked the originals game and continues to give traditional Hollywood studios a run for their money. While licensed content will continue to play an outsized role, originals help unlock additional monetization opportunities such as theatrical releases, product placements, and merchandising.

Netflix expects a significant jump in its free cash flow at $6.5 billion, resulting in lower content expenses. In fact, they expect to spend $14 billion on content next year, down from $17 billion which will surely increase cash flow. This has prompted the company to increase its buyback authorizations by $10 billion, creating plenty of support for the stock. The company ended the quarter with $8.6 billion in cash, $17 billion in debt, and $4.6 billion in cash flow. The stock has been hit hard these past five weeks, for conceivably no good reason, as this quarter shattered expectations. This company remains one of our favorites. Our Target is $590 and our Sell Price is: We would never sell Netflix. Yes, the Target is high. But yes, the stock will get there. 2024? 2025? It WILL get there. The competition is shattered and will have to consolidate, with Netflix the clear winner.

by Todd Shaver | Sep 29, 2023 | Instant News Flash

The valuation of automaker Tesla (TSLA: $252) has long been an enigma for Wall Street and the company continues to astound and astonish analysts to this day. The stock was considered overvalued when it first went public in 2010, with a valuation of $2.2 billion, just as it is today with a market cap of $760 billion. And in the preceding years, many short-sellers have lost fortunes trying to bet against the company. We have a personal friend, a former Merrill Lynch VP who ran an office in Florida, who has been short for the last four years. He has lost over seven figures. We have implored him to buy back the stock, especially when it went to $102 in January of this year, down from the all-time high of close to $400 set in late 2021.

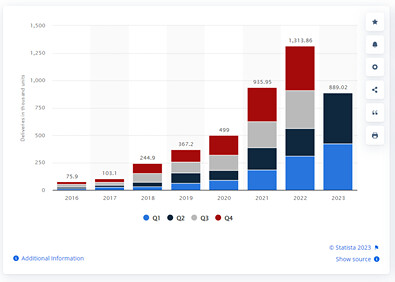

To be fair, it's hard not to question the exuberant valuations that the automaker has consistently held, which is 16 times the market cap of Ford Motors, a 120-year-old behemoth that sells twice as many cars as Tesla, and three times that of Toyota, which currently sells 10 times as many cars. Even considering Elon Musk’s ambitious goal of making 20 million cars a year by 2030, the valuations are a tough sell, particularly in the face of rising competition. The company is on track to deliver 2 million this year, up from 935,000 two years ago.

Number of Tesla vehicles delivered worldwide

Tesla has remained the most popular stock among retail investors for years. While it is also the most shorted stock as of now, with over $21 billion in short interest, the fate of these shorts looks increasingly shaky, similar to the many institutional, retail, and hedge fund bets made against the stock over the past decade. And as you know quite well by now since we have mentioned this numerous times, having a large short position is very bullish. Why? Because the only thing shorts can do is to BUY BACK their stock, which pushed the stock higher.

As discussed in our research report when we first began covering the stock two months ago, Tesla is not an automotive company, and it would be a mistake to value it as such. With its ambitious plans to flood the streets with robotaxis, its Dojo supercomputer that the Street estimates to be worth over $500 billion, the massive battery factory in Nevada, and innumerable other innovations, rather than an “automotive” company, this is a high-growth tech company through and through.

Reuters said this eight days ago: “Tesla has drawn up plans to make and sell battery storage systems in India and submitted a proposal to officials seeking incentives to build a factory, as Elon Musk continues a push to enter the country. Tesla has been in talks about setting up a new electric vehicle factory in India to build a [world] car priced around $24,000 for weeks, with discussions overseen directly by Prime Minister Narendra Modi.” We have heard that Tesla has plans for another large battery plant as well.

Another overlooked asset is the company’s extensive network of 45,000 superchargers, which it has yet to monetize. Most competitors have adopted Tesla’s North American Charging Standard. Rising competition and growing penetration of EVs on American roads only stand to benefit Tesla going forward.

Tesla is not just an automobile manufacturer; it is the future of mobility, computer vision, and sustainable technology, all rolled into one. Its vision-based AI system has applications beyond mobility, similar to its growing prowess in battery technology. With robust tailwinds across the board, and a well-capitalized balance sheet with $23 billion in cash, just $6 billion in debt, and $14 billion in cash flow, we believe that this company, with a market cap of $800 billion, run by an acknowledged genius, is poised to continue to change the world as we know it. Our Target is $325.

If you are still not convinced, get the new book called Elon Musk, by Walter Isaacson. We read all 615 pages in three days this week. He is changing the world that we live in.